TLT Trade Idea

TLT Trade Idea

PCE Heats Up, Long TLT Trade in Play: Macro Snapshot

Hey guys,

It’s been another one of those busy weeks.

Markets, updates, and a few in-person conferences as well— nevertheless I made sure to get this report across on time.

We’ll be going into the recent PCE data, the rising liquidity concerns and how that plays well into our long TLT trade idea.

Before we do that, let’s run through our macro snapshot, thought of the week and chart of the week.

Enjoy ;)

The Macro Snapshot

It’s already on everyone’s mind so I’ll just say it…

More of this PCE data and we’ll be having conversations about the potential return of the Fed hike— we’re not yet there, but a consistent flurry of hot CPI print will eventually raise this question at future FOMC press conferences.

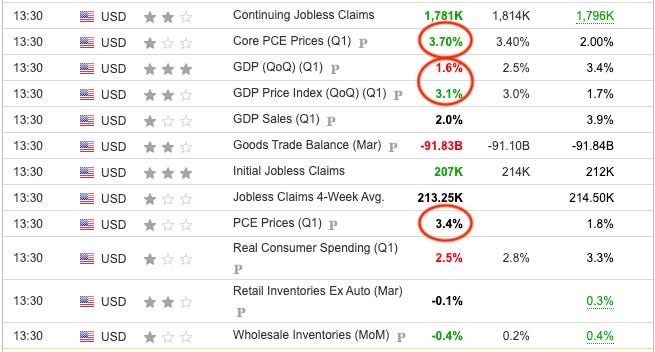

Highly anticipated GDP & PCE data for Q1 was released this afternoon and it’s safe to say that markets weren’t too pleased with the print. Core PCE rose 3.70% in Q1 vs forecasts of 3.40%, whilst GDP slowed to 1.6% vs 2.5% expected. This was the slowest pace of growth in 2 years, on the other hand, PCE inflation accelerated back to Q2 ’23 levels.

Market’s result?

Sell-off across bonds (bearish rates), equities and a firm reaction in Fed cut expectations which we’ll touch upon below.

Thought of the Week

A tapering in the Fed balance sheet runoff means one thing.

Reduced selling pressure on rates resulting in a yield compression (lower rates), that presents strong treasury opportunities, particularly on the 2s and 10s. Rates on the 2s are yielding 4.995% whilst 10s are at 4.70%.

Post-PCE rates have experienced further selling pressure, this improves the overall risk/reward balance of a short treasury position.

Chart of the Week

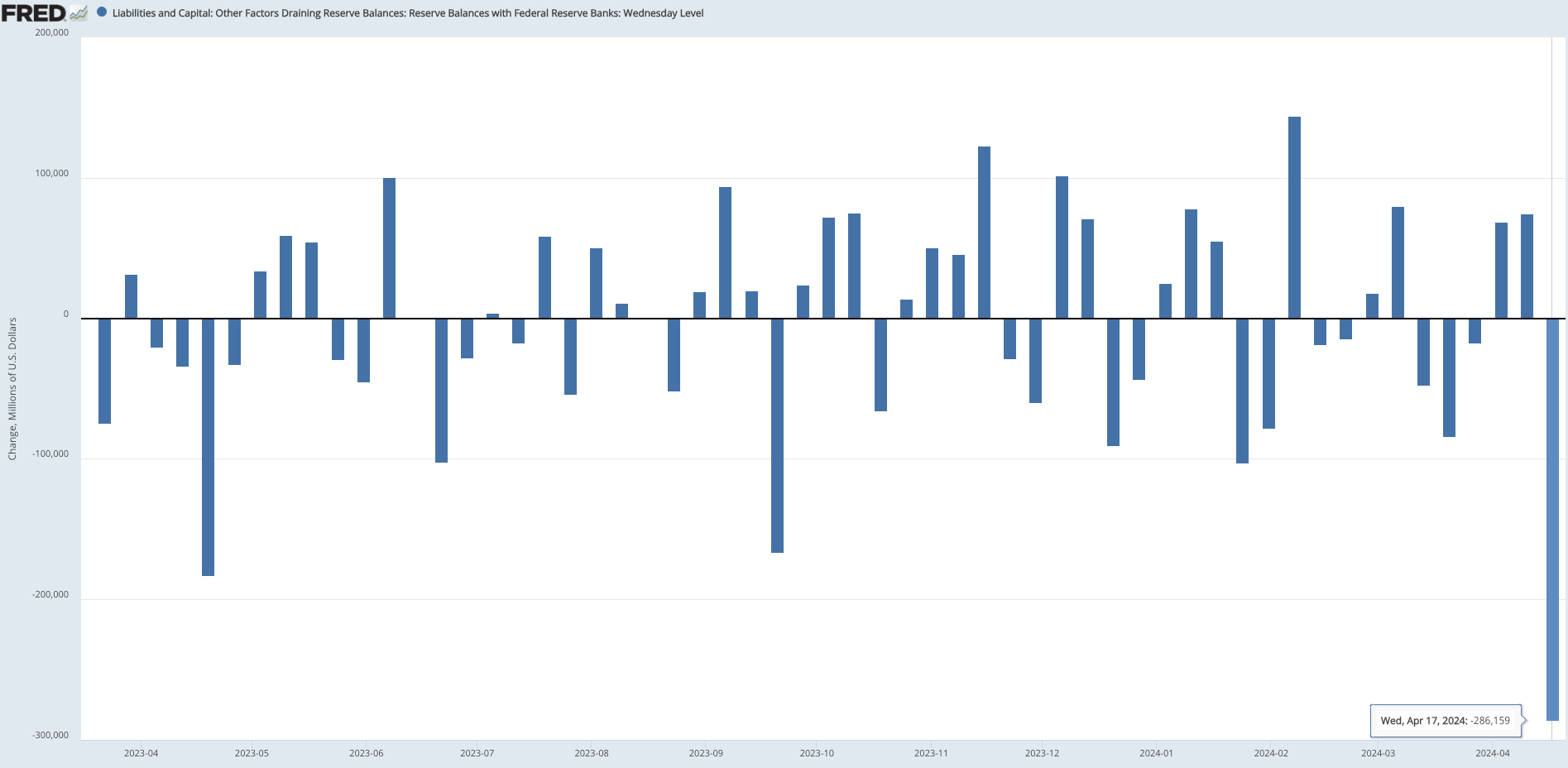

Financial Flow of the April Tax Week

Last week was tax week in the U.S— and roughly $300b in reserves left the banking system as taxpayers made tax payments to the Treasury, which resulted in a boost in the TGA (Treasury General Account) which if you’re unaware, is basically the bank account for the U.S government (seen below).

This shift in capital, although widely anticipated, can have vital impacts on financial markets. The main factor at risk here is liquidity.

Reduced liquidity has a number of implications, we’ll look at the two main channels:

Unwanted tightening of credit conditions: With lower reserve balances, banks instantly become more cautious about lending capital. This reservation is expressed through tighter interbank market credit conditions.

Repo operations: The Fed may look to utilise its repo operations (repurchase agreements) to temporarily provide reserves to banks, or instead of using this channel they may look to expedite the process of tapering their bond runoff program.

Long TLT Trade Idea

Time Horizon: 6 months

Rates have been bearish since the start of the year despite the dovish narrative of a Fed cut dominating mainstream media throughout the early part of January.

The Fed is set to announce a slowing of their QT, which has seen the RRP (reverse repurchase agreement) market decline from $2.2 T in April 2023, to roughly $400b in April 2024. This large reduction in the RRP raises the risk of a liquidity shock amongst banks and financial institutions which the Fed doesn’t need, especially within an election year which would further complicate things even more.