The Resurrection Of The Fed Hike?

The Resurrection Of The Fed Hike?

Breaking down the hot PCE print and the implications on the Fed

Hey everyone,

I spent the week learning new aspects of global macro.

It’s intense.

But that’s the beauty of this game.

You learn, and you then learn how much you don’t know, that’s why I started this journey— to fill the gap in knowledge between skilled money managers and a relentless kid with a passion for global markets.

It’s 18º in London, meaning I’ll be going for a walk by the time you’re reading this later this evening. It helps unclog my thoughts.

Anyways, Germany entered a recession early this week after Q1 growth for the nation came in -0.3%, a second consecutive negative quarter. Today U.S PCE surprised us to the upside so I’ll unveil what this means for markets.

As always, lend me your attention:

The Fight Isn’t Over: PCE

Last week Jay Powell spoke at a conference where he emphasised that being data-dependent was the only way forward.

And surprisingly, markets seemed to believe his comments, pricing in a pause at the upcoming Fed interest rate decision on June 14th. However, today’s PCE print has put investors back on edge in regard to the Fed’s next move. Markets, however, don’t seem to be too bothered by the high PCE print we saw; it’s green all around, equities, commodities, even crypto. So let’s take a look beneath the hood and see the breakdown of PCE.

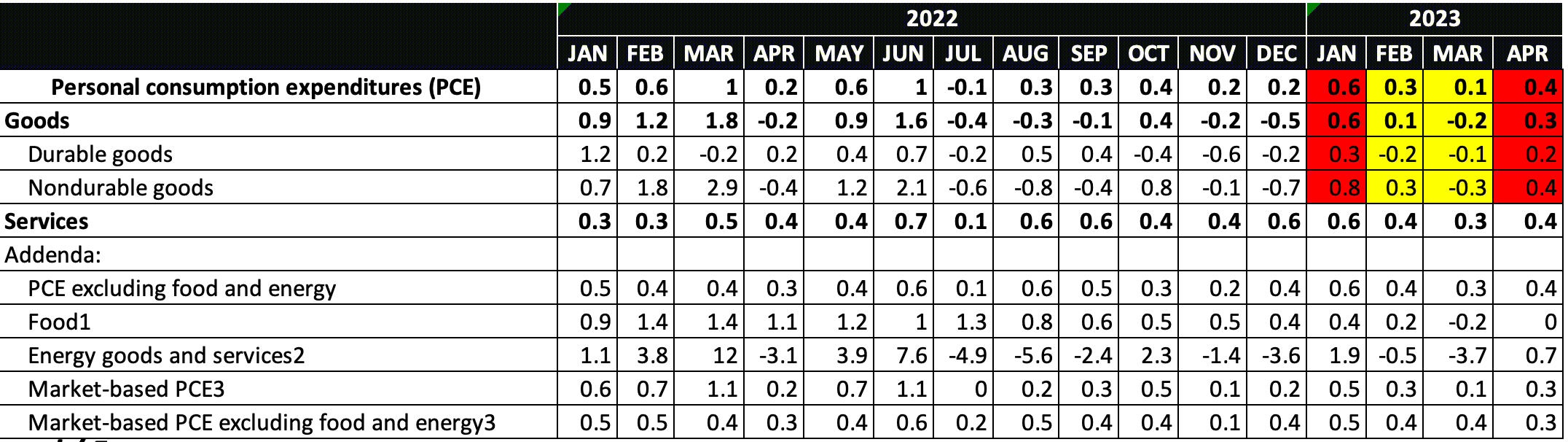

PCE by composition

I purposely chose to colour code the PCE readings year to date to represent soft readings (yellow) and hot readings (red). Starting the year off, January’s PCE print came in hot vs the expectation of 0.4% which warranted the Fed’s 25bps hike in March amidst the banking scare.

Now to briefly explain for those that aren’t aware, the Fed’s priority inflation measure isn’t CPI, it’s PCE, and there’s a reason for that. The PCE reading is much more sensitive to changes in consumer spending habits due to its weighting and calculation methodology. You see the PCE measures a wider range of goods and services than the CPI whilst also measuring the things that consumers actually purchase vs the CPI which only measures a fixed basket of goods set by BLS.

Meaning?

That fixed basket of goods is not a true representation of the inflation consumers are actually feeling, the BLS basket is updated every 12 months whereas PCE is updated quarterly according to what real consumers are putting in their baskets.

Now, back to figure 1, both nondurable goods and energy goods added 0.4% and 0.7% for April. Concerning right?

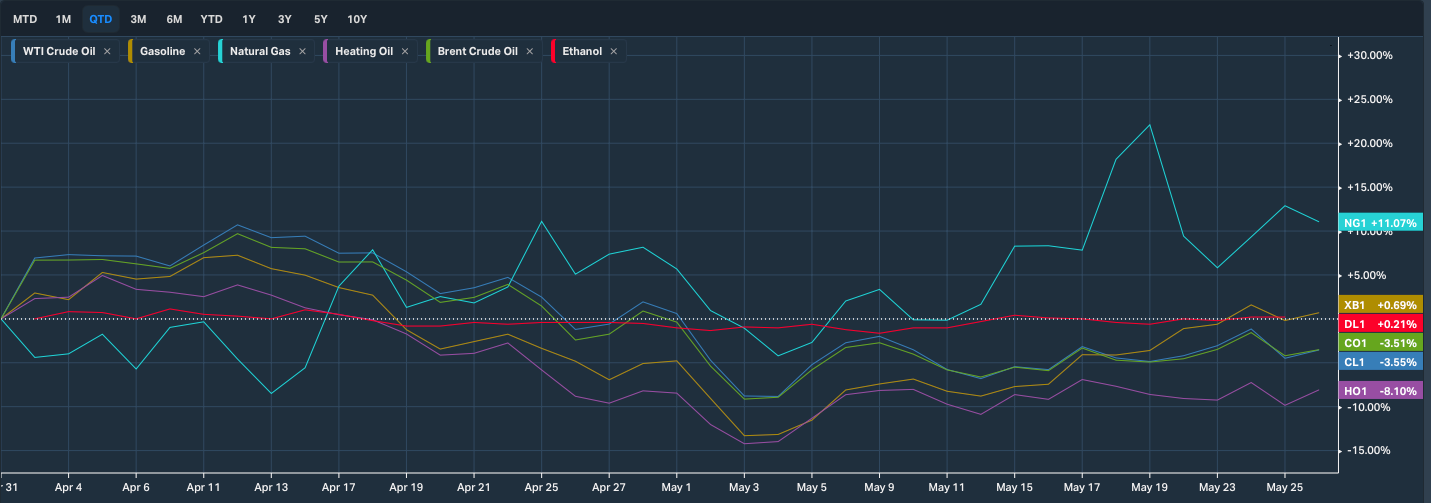

During April, commodity prices fluctuated +/- the 0% mark with naturals being the only strong driver of high prices amongst the energy-based commodities; looking forward we can see that gasoline, heating oil, ethanol and Brent are all on their way up above the 0% price change mark.

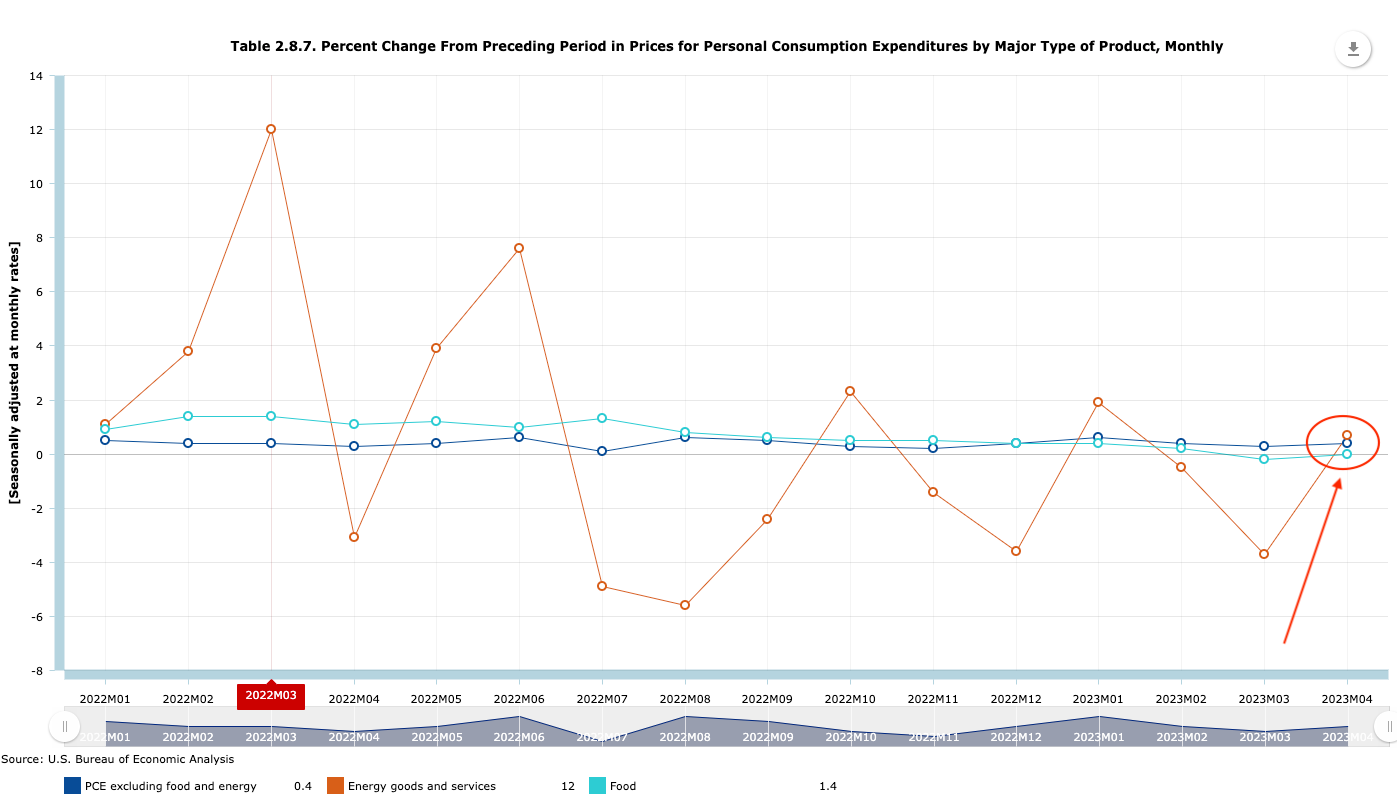

Figure 2 shows the volatility that energy goods and services have added to the reading, rebounding from -3.7 in March to +0.7 in April. Considering the season we’re set to enter we could see sustained increases in energy goods and services keeping the PCE figure at a halt.

There are several reasons for the rebound in energy prices. One is that in the U.S, Memorial Day (Monday 29th of May) marks the start of the summer travel season for U.S citizens, resulting in increased cost of fuel prices as citizens begin their summer road trips around the country pushing fuel costs higher.

Now aside from the Memorial Day fuel pressure, earlier in the week Saudi’s minister of Energy Abdulaziz Bin Salman was quoted warning that anyone shorting oil would be left “ouching” and giving a reminder that they should “watch out”.

Something that I mentioned in my private report for members earlier yesterday. The worry here is that this sends a message to market participants that OPEC is set to announce cutbacks in oil production in order to squeeze the global supply pushing oil prices higher.

My bias on crude is short, but now transitioning to neutral upon the OPEC meeting set for June 3-4 in Vienna.

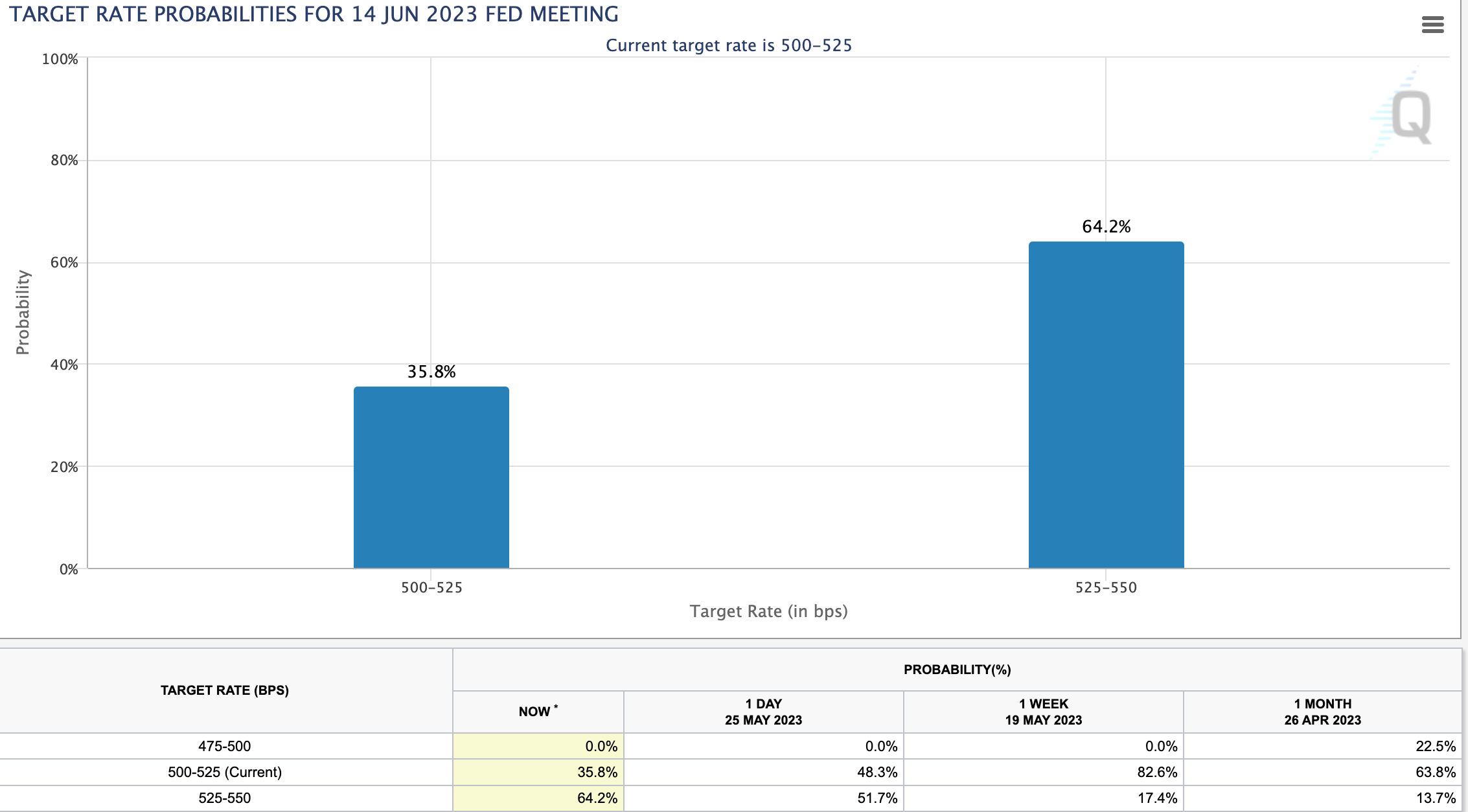

All of the above puts additional pressure on the Fed, remain data dependent or hike in June? Just 1 week ago, markets had the chance of a Fed hike at 17.4%, now that figure has jumped to 64.2%!

The question is simple. Will the Fed hike?

After today’s data print. I’ve got a 40% conviction that a 25bps hike is on the table for June; which is a complete reversal from where I was seated a week ago. With NFP set for next week Friday, if we see another tight labour market print then I think the probability of a Fed hike would rise past the current 60%, however, with everything, conditions change.

19 days to go is a long time for the pendulum to swing either way, the main hurdle for the U.S right now is signing off on their debt ceiling limit which is closing in as soon as June 1st.

Thanks for getting to the end of this piece.

I’m back at the drawing board from tomorrow to improve the quality of both my deep reports and brief summaries like this one for you all.

I’m always keen to hear what you think so let me know in the comments!

Until next time