The Oil Update: Balancing Demand, Supply & China

The Oil Update: Balancing Demand, Supply & China

China's Economic Struggles Cast Shadow on Crude Prices, Investment Neutrality in Short Term, Bearish Long Term

Hey crew,

It’s been another fruitful week.

Each step forward reinforces the next, and the next, and the next. It’s a spiral wheel of increasing self-belief.

I encourage you to seek opportunities that force you to grow into a better version of yourself.

A mentor of mine I’ve never met said this:

“When faced with new information, don’t revert to old instincts. Change”

Anyways, today we’ll be covering a key look at what’s shaping the global macro landscape. It’s been a while since a deep dive into the world of commodities so here we go. As always, grab a pen, and paper and take notes.

Oil Markets Developments

Crude Oil House View: Neutral/Bearish

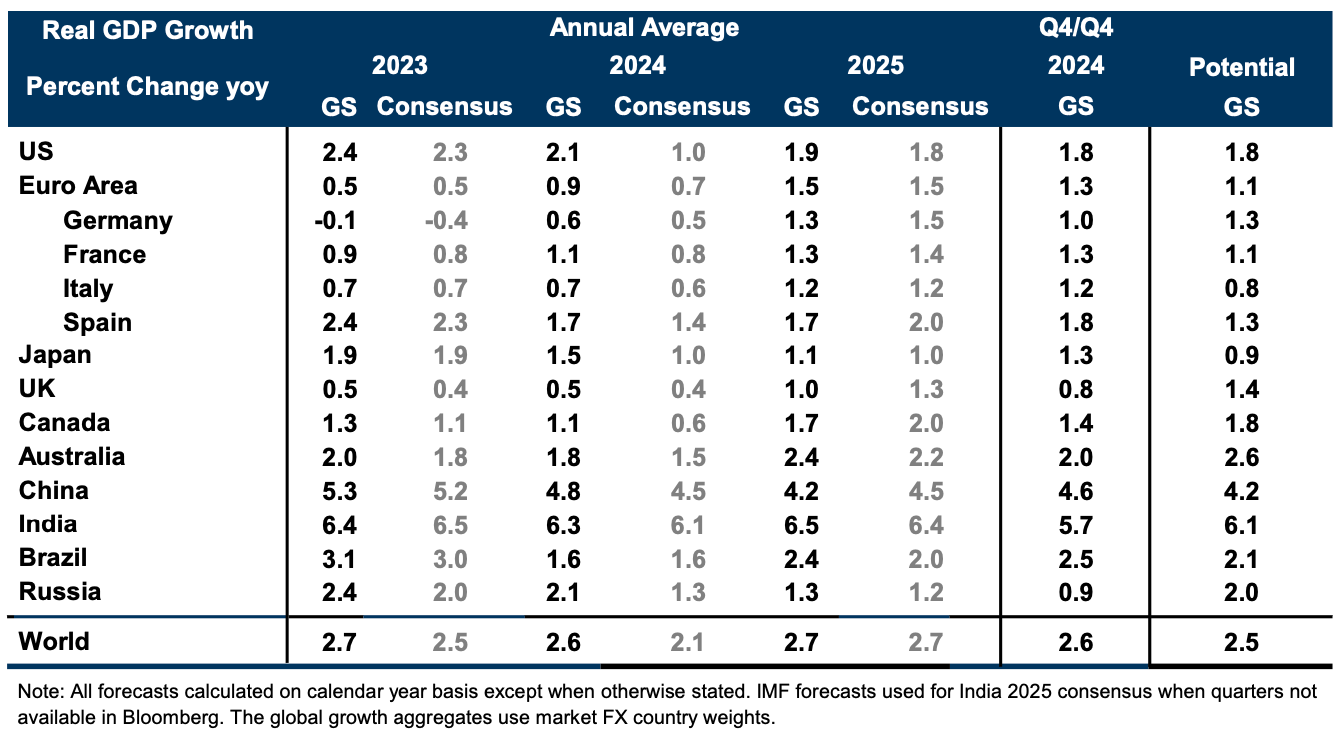

World Growth

Global growth is a key attribute to the performance of Crude oil prices. Although there are many factors which can affect the price of crude such as geopolitical tensions, the market boils down to the fundamental trend of global growth which drives supply-demand dynamics.

For many of us, including investors, global growth in 2023 outperformed our forecasts and expectations. For one, was quite pessimistic about the dollar's performance against the G10 basket. However, the Biden administration's stimulus package, including measures like the IRA (Inflation Reduction Act), triggered a surge in US growth pulling the rest of the world further.

Looking forward, global growth is expected to grow by 2.7% according to GS, which is aligned with several Wall Street banks’ estimates.

The U.S is expected to continue with its economic strength growing by 1.9% in 2024.

World Oil Demand

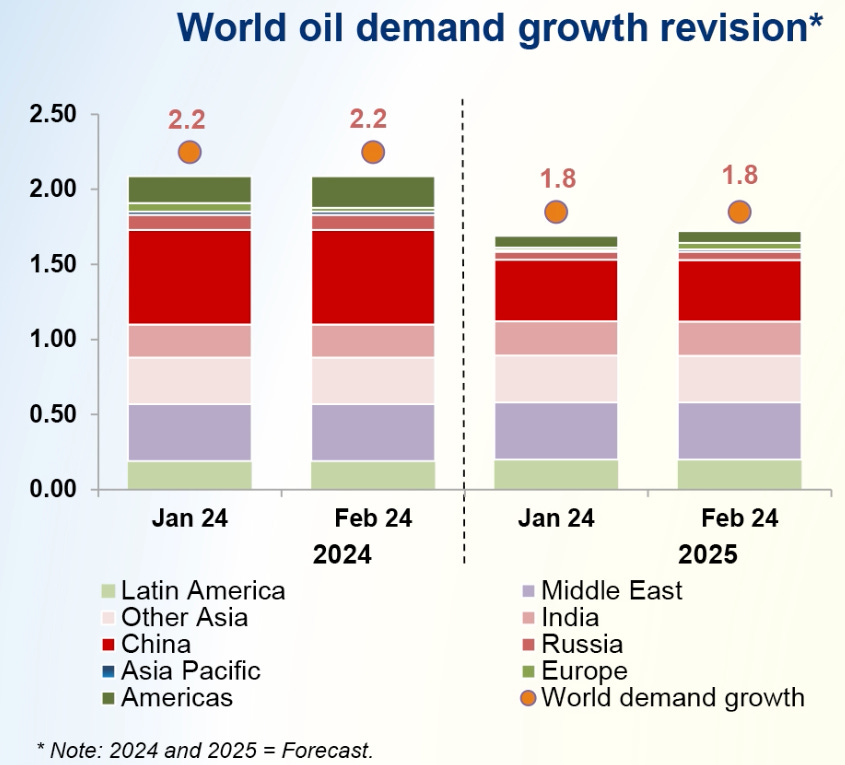

As we know, the largest consumer of crude products is Mainland China, which unfortunately has been experiencing structural and economic weakness across the economy over the last 5-6 years mainly, stemming from the introduction of tighter capital controls in 2016 and the trade war between US-China encouraged international companies to de-risk away from China. The restrictions now limit individuals to exporting only $50,000 annually, further dampening economic activity.

Figure 2 depicts OPEC's recent revision for global oil demand in 2024 and 2025, predicting a flat trajectory. This raises a crucial question: is the current oil market in equilibrium at its prevailing price? While I'll address this later, let's delve deeper into China's economic outlook, represented here by the "large red stack." Structural issues weigh heavily on both domestic and foreign investors. The Chinese economy's diminishing dominance in global low-cost trade, with the rise of competitors like Vietnam, adds to concerns. Furthermore, the "balance sheet recession" – where consumers prioritise debt repayment – and the property sector's struggles (accounting for nearly 20% of GDP and facing widespread developer defaults) further dampen the economic outlook.