The Interbank Meltdown: Repos

Hey MMH team,

It’s March.

Keep swinging the bat.

2/12 rounds are done, make a promise to finish strong this year.

I thought I’d bring a report out of the archive and refresh it with the help of

, the intermarket specialist.Many of you fail to recognise the crucial role the interbank market plays in broad financial markets, so let this report bring awareness to your understanding of this rather undisclosed market.

Deconstructing the Interbank Money Market

The interbank lending market, aka interbank money market, is not widely discussed in mainstream finance media. There’s one main reason why in my opinion, it’s deep complexities. The interbank money market is a highly liquid global market where banks and shadow banks can borrow from each other to meet liquidity needs.

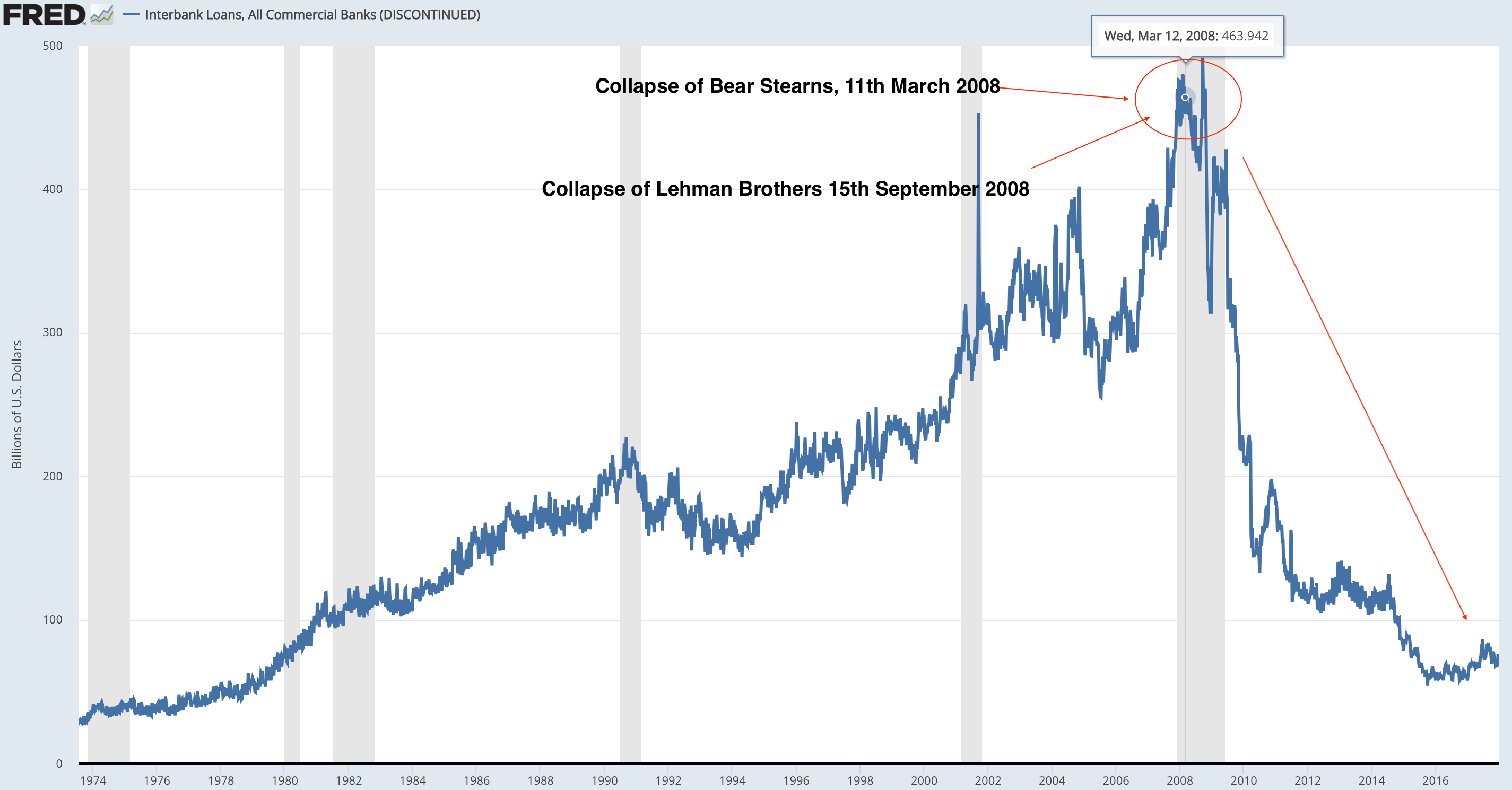

Firstly, to understand the structure, importance and changes within the interbank lending market, we must revisit the market crisis of 2008.

The global financial crisis of 2008 highlighted the crucial role of interbank lending markets in the financial system and wider economy. The collapse of large institutions Bear Stearns and Lehman Brothers revealed one thing, in times of crisis the interbank lending market becomes an important channel of contagion. The collapse of two banks instantly shocked the money markets, market rates for lending rallied through the roof whilst transaction volume significantly decreased. As with anything, the level of distress in money markets caused credit supply to the non-financial sector to drop substantially, effectively tightening financial conditions for the wider economy, resulting in the highest levels of unemployment last seen in the 80s and recently during COVID-19.

The consequences for the financial sector was an array of strict, and tough regulations mainly brought upon the banking sector to mitigate the event of another ‘liquidity crisis’.

Regulations such as the Basel III came into effect post-GFC in 2009; its main function was to discourage systemic risk and leverage with markets.

As always, I aim to break down the complex jargon into simple layman’s terms to make reports easily digestible, so let me explain what is meant by systemic risk.

Now, systemic risk is the dark side of having a deeply interconnected financial system. It’s the risk that a problem in one part of the financial system could spread to other parts and financial players causing an '08-like collapse. Contagion risk. A term you should be familiar with.

During the GFC, subprime mortgages were at the heart of the systemic risk, and these unworthy credit instruments were widely adopted by financial institutions, meaning one blow-up led to a widescale blow-up of subprime mortgage portfolios across the street.

What purpose does the interbank funding market serve?

As the name suggests, this market provides immediate access to short-term liquidity requirements.

How?

Through money markets. Money markets offer two forms of lending: secured and unsecured. Secured lending, such as repurchase agreements (repos), is collateralized, while unsecured lending is not.

New regulations have disincentivised banks, especially systemically important banks (SIBs) such as JPM, and Citibank, from lending to each other, leading to a decline in bank-to-bank lending.

As you can interpret from the chart, the collapse of Bear Stears and Lehman sent ripple effects throughout the financial system which systematically changed the risk appetite for interbank lending forever.

On the other hand, the repo market has seen an increase in transactional volume as non-banks absorb the risk banks once took.

“the interbank market plays crucial roles in domestic financial systems because first, central banks intervene in this market to guide policy interest rates, and second, efficient liquidity transfer can occur between surplus and needy banks through a well-functioning interbank market”

— ECB, The interbank market puzzle report

This excerpt highlights the importance of the money market, which central banks use to implement monetary policy. By engaging in repurchase agreements (repos) to inject liquidity or reverse repos to withdraw liquidity, the Federal Reserve plays a significant role in shaping credit conditions via money markets.

Between the two forms of lending (unsecured and secured), the repo market (secured) generates the largest volume of transactions due to its greater liquidity and a wider range of market participants including banks, money market funds (MMFs), government-sponsored entities (GSEs) and of course lower risk. So when looking deeper at the world of collateral two things are clear, the availability and quality of collateral are vitally important.

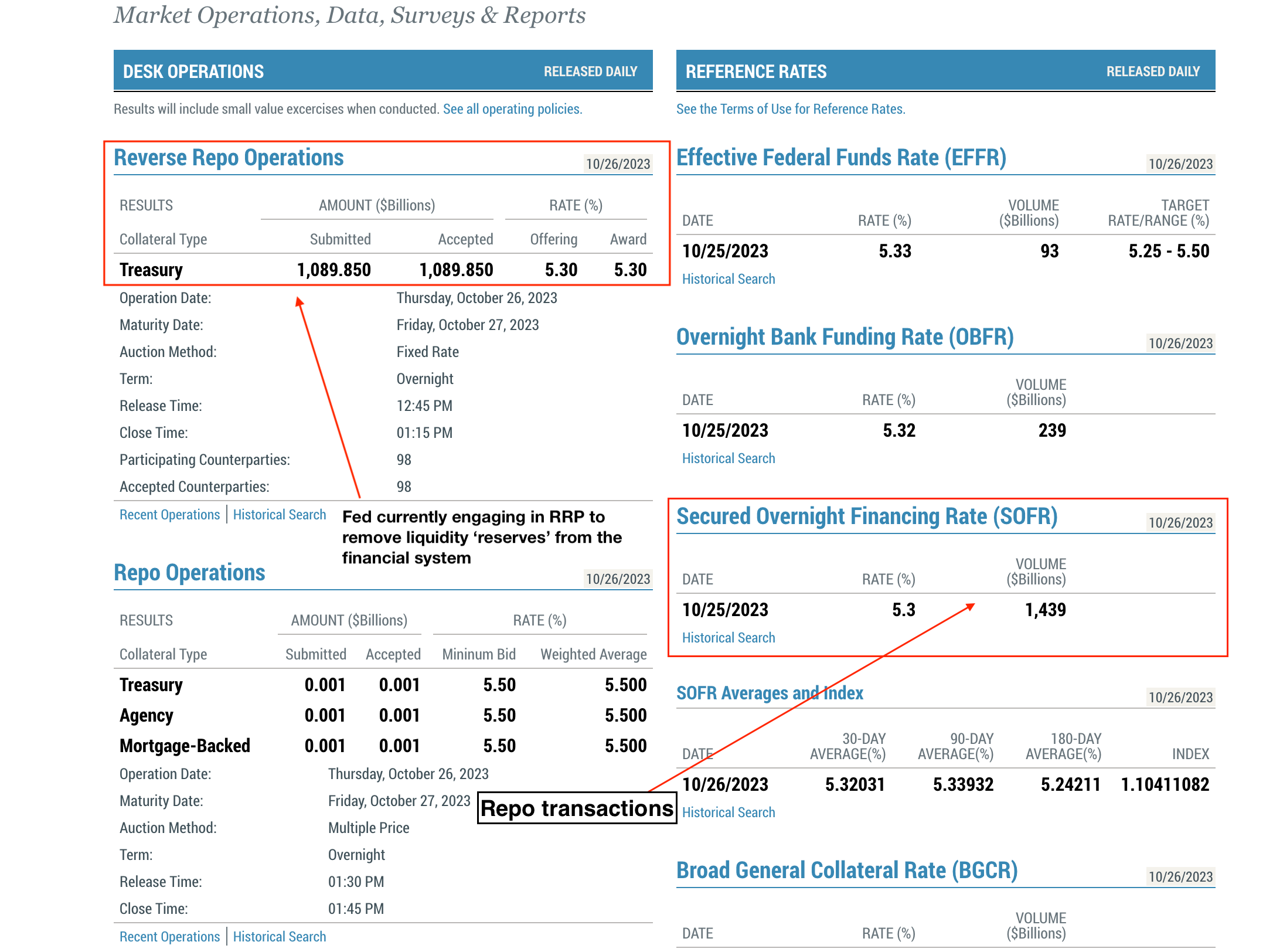

Following on, it’s equally important to know what factors affect the availability of collateral and SOFR rates, which is the rate for secured overnight borrowing. From a policy perspective, the Fed’s OMO (Open Market Operations), QE & QT are the main factors which could affect the stability of the interbank market.

The data dashboard above first signifies the size and depth of the secured overnight funding market (repo market) when comparing the daily volume to that of the OBFR and EFFR, which are both unsecured overnight funding markets.

In the top left corner, I have highlighted the reverse repo operations that the New York Fed has been conducting to reduce liquidity in the financial system as the Fed rolls off securities from its balance sheet as part of its quantitative tightening program (QT). During quantitative tightening programs, the Federal Reserve Bank of New York's market dashboard will typically show the Fed accepting propositions to loan out reserves, as illustrated by the chart above. This is usually where people get slightly confused, as during QT, the aim is to drain reserves not supply them right?

Yes, but a key part of the reverse repo facility is that the money market fund will have to purchase the collateral, usually US treasuries, from the Fed after the duration of the loan at a higher rate— resulting in a net reduction in reserves from the financial system.

Secured Interbanking Funding Market and Broader Economic Fundamentals

There’s more than that. Secured interbanking funding market is like a spider web. In the centre, there are central banks “pulling the strings” trying to impact financial conditions. But more importantly, there are Primary Dealers (the likes of GS, JPM, BofA…) distributing collaterals and funding through to other market participants “further along the web“. In other words, the Primary Dealers are the important “knots“ making markets between buyers and sellers of secured funding.

Being in the centre of the web for decades they learn a thing or two about the markets. They have the most savvy repo traders who keep a close look at the market trends, making sure that the haircuts rates on the secured funding are fair and able to fend off any risks.

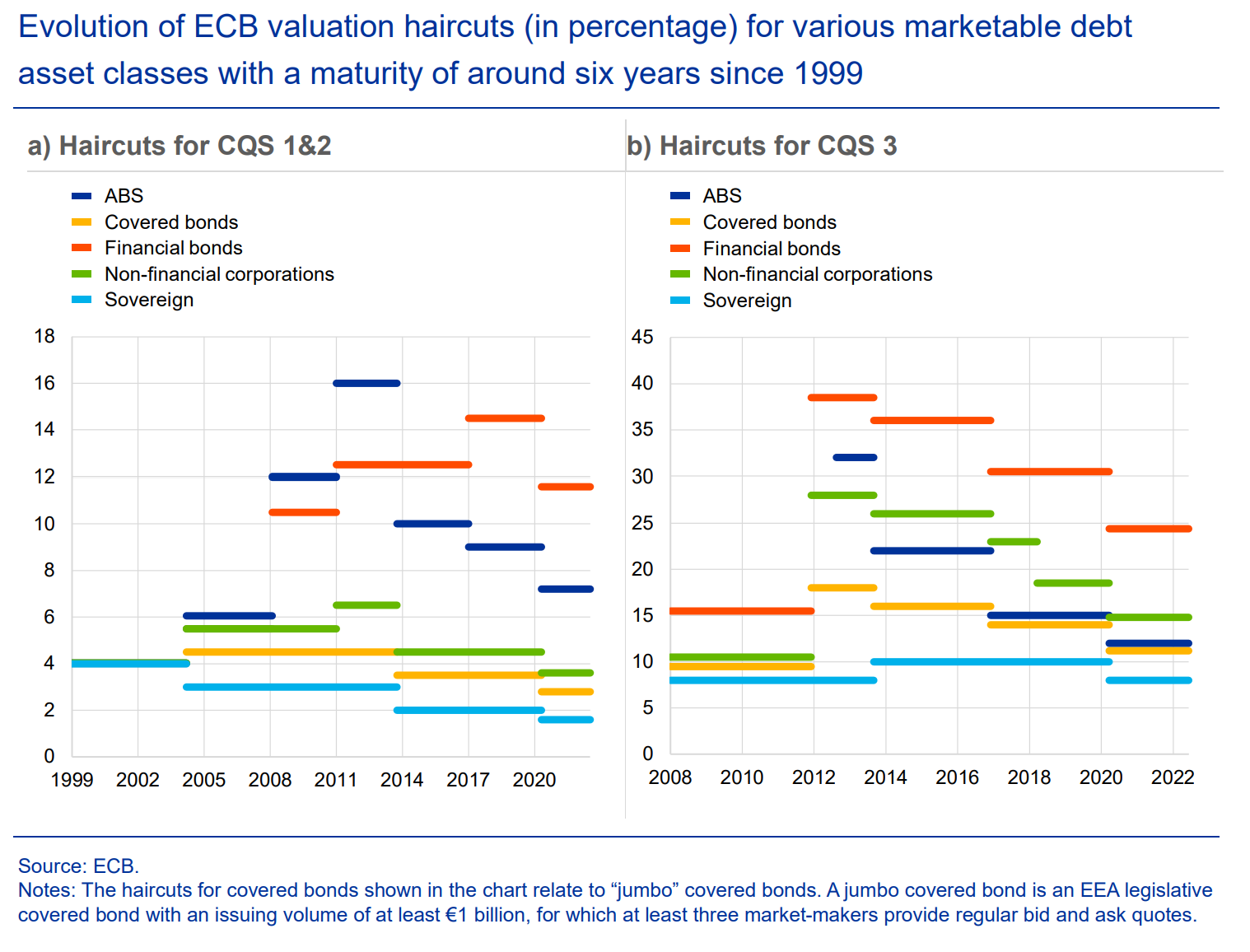

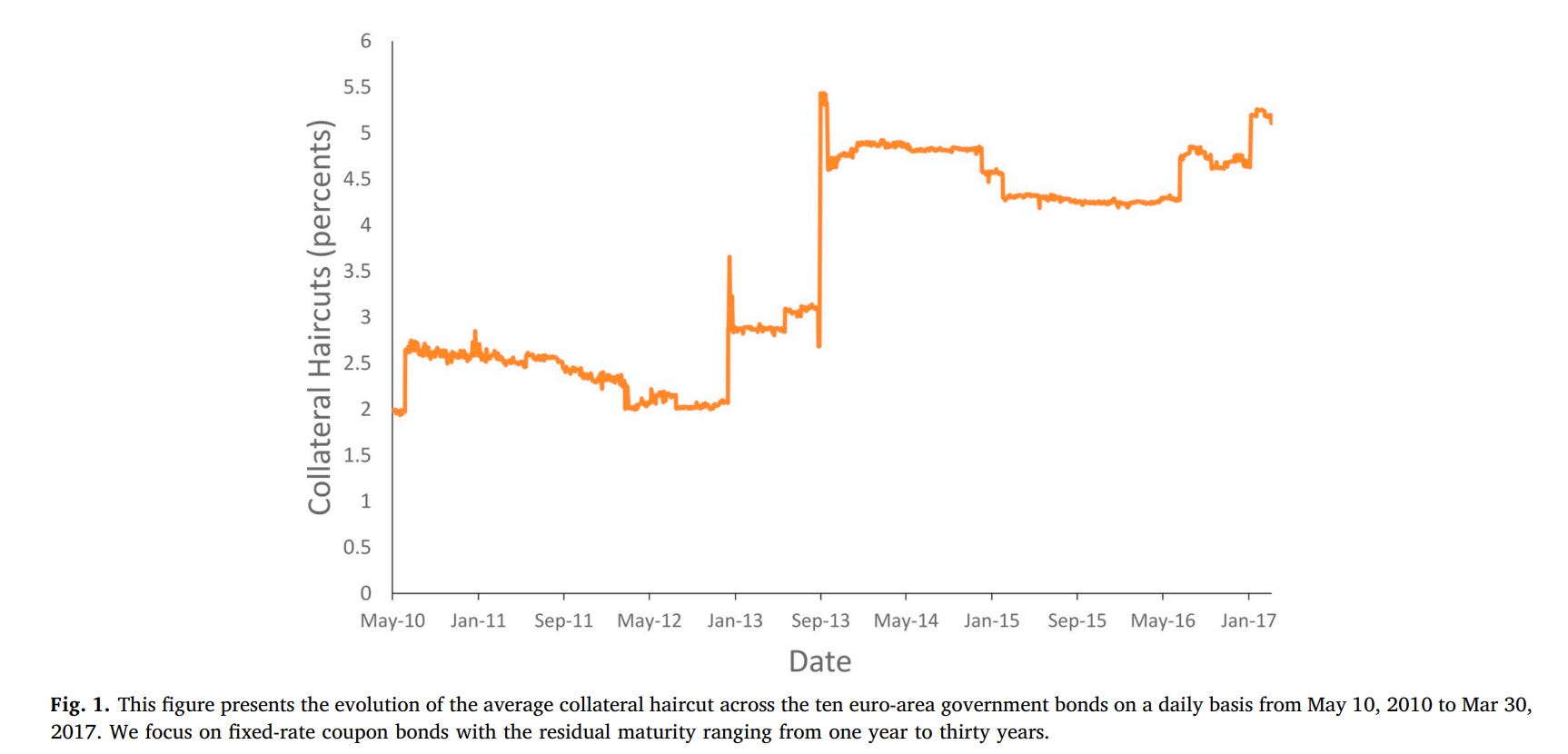

Hold on what is a haircut rate? Put simply, it is a percentage deducted from the market value of the collateral to determine the amount of cash that will be received. For example, if a security is worth $100 and the haircut rate is 5%, the borrower would receive $95 in cash. This discount, or "haircut," serves as a protective buffer for the lender against the risk of the collateral's value declining before the repurchase is completed.

Traders are sharp and wary, so when there is any sign of uncertainty or crisis, they became alert and quickly raise the haircut on repo transactions that are not safe. Simply look at the haircuts:

source: The valuation haircuts applied to eligible marketable assets for ECB credit operations (europa.eu)

source: Nguyen, M., 2020. Collateral haircuts and bond yields in the European government bond markets. International Review of Financial Analysis, 69, p.101467.

Notice that the haircut rates (especially of the more “risky assets“) skyrocketed during the crisis. For example amid GFC and European Debt Crisis there were notable spikes in the haircut rates for ABS, covered bonds. In this respect, collateral haircuts could serve as an early indicator of economic cycles, enriching our investment analysis and allowing us to “time“ the market more efficiently.

Conclusion

From this report, I hope to have explored the progression of the interbank market from the GFC crisis and explained the relationship between monetary policy and the overnight financing rates, as well as how it relates to the boom and bust of economic cycles. As broken down in this report, the extensive regulation has pushed banks away from the lending market to avoid systemic risk whilst attracting the likes of shadow banks. The interbank market has many more moving parts and complexities which I aim to break down for you; as for now, I hope you enjoyed this rather educational insight into the interbank world.