The G4 Review (Pt.2)

The G4 Review (Pt.2)

Eagerly Awaiting The Cut...

Hey Crew,

It’s been one intense week.

Some groundwork is being laid at MMH.

I’ll update you soon.

For now, enjoy Pt.2 of the G4 Central Bank review:

Fed Pivot on Hold: Dot Plot

On Wednesday the Federal Reserve maintained its benchmark interest rate within the 5.25-5.50% corridor. The nuanced tone adopted by the Federal Reserve signalled a potential deceleration in quantitative tightening measures.

Notably, Chair Jerome Powell exhibited resilience in the face of elevated inflation metrics observed in January and February 2024, allowing an overarching bullish sentiment to continue fueling financial markets and causing an uptrend in asset valuations.

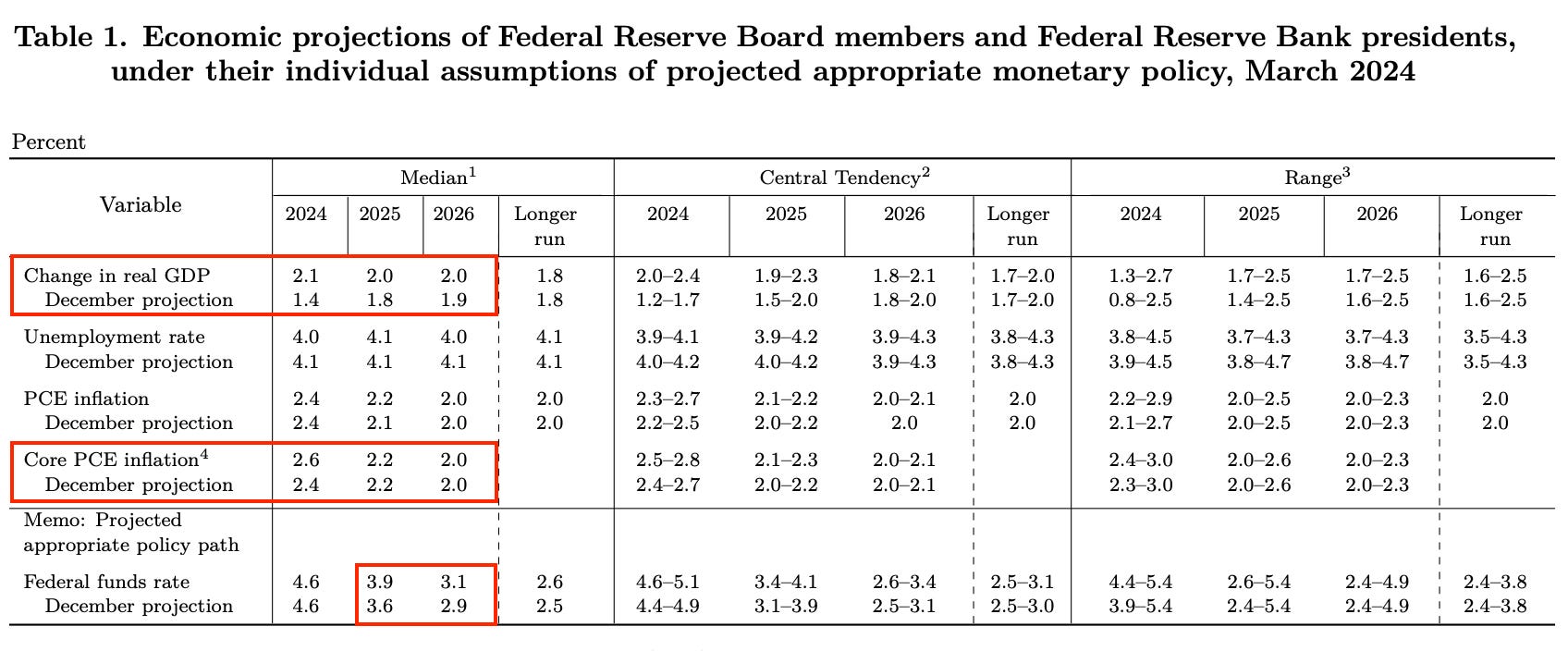

Market expectations had already priced in a hold, shifting the focus to the Statement of Economic Projections (SEP). The SEP revealed a more robust economic outlook from the Federal Reserve, surpassing forecasts from December 2023. The revised benchmarks reflect enhanced growth prospects, rising inflation, tightening labour markets, and a higher neutral interest rate of c.2.6%.

While the SEP highlighted a more dynamic labour market, Chair Powell reiterated the Fed's commitment to potentially reducing rates later this year (dovish tilt).

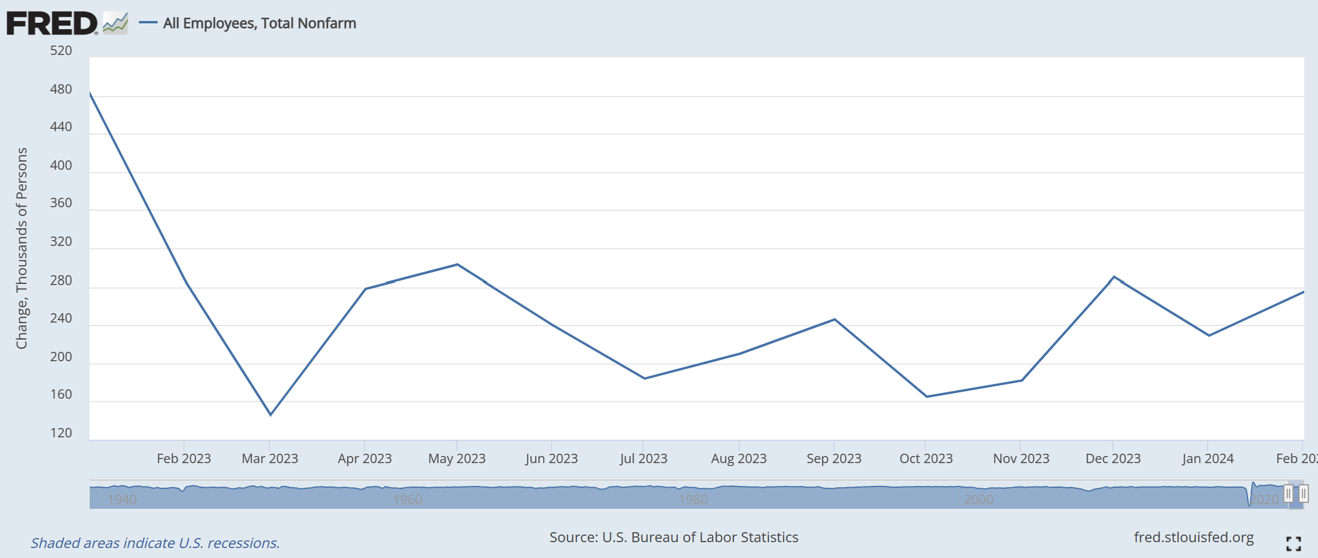

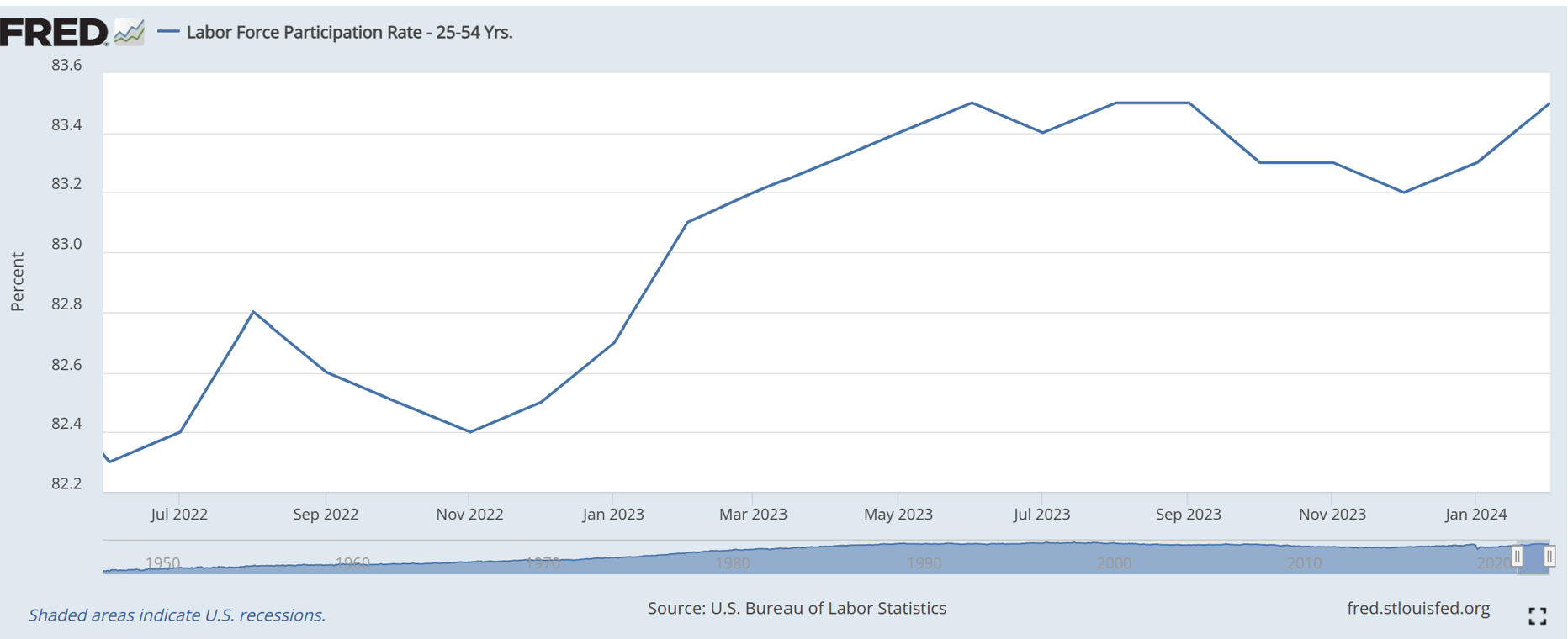

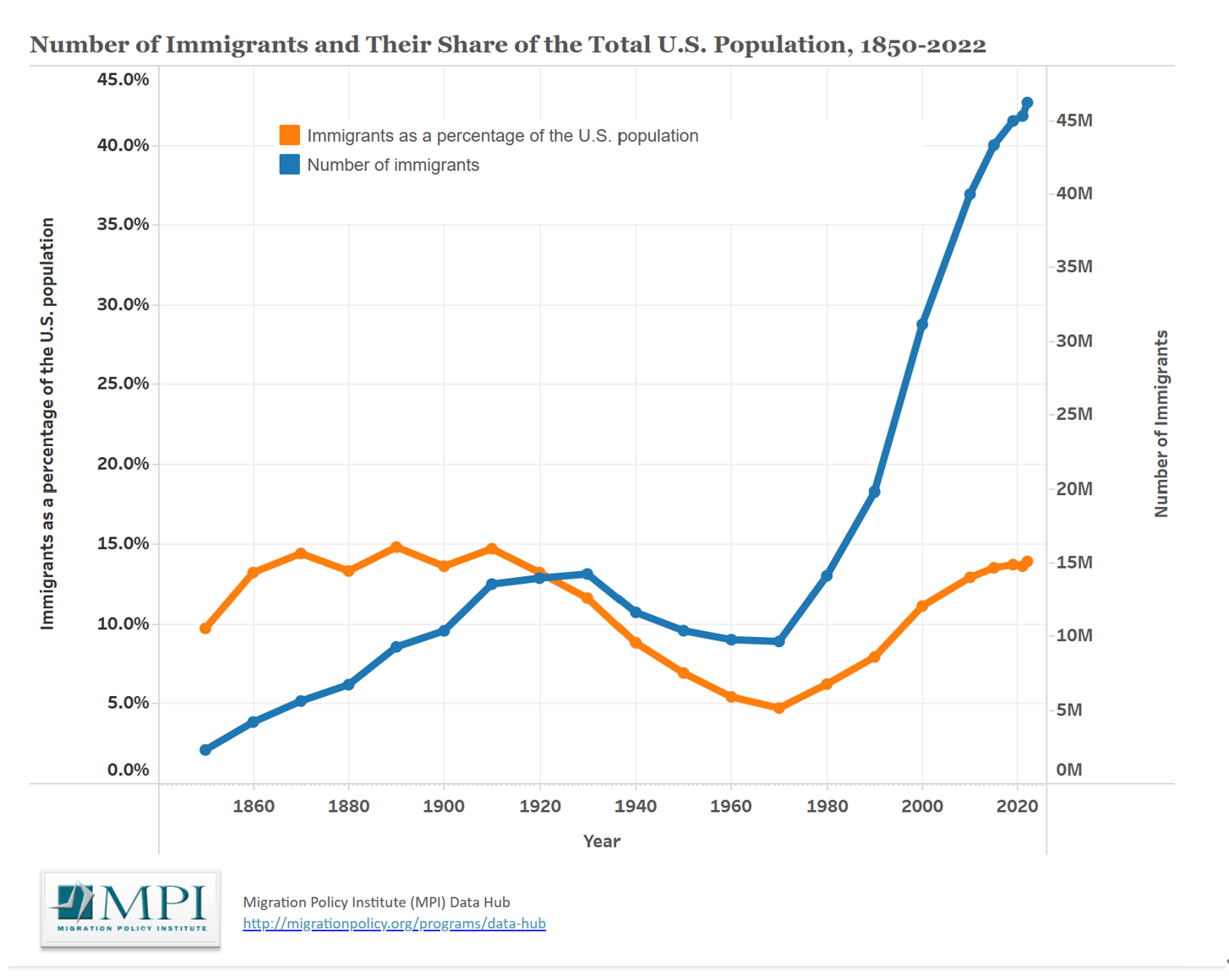

In December's FOMC meeting, markets interpreted the Fed's policy stance as a long-awaited pivot. Expectations for a rate cut at the March meeting surged immediately. So coming into the new year markets were waiting for the future shift towards monetary easing but were hit with economic strength pushing the cuts further down. The strong labour market, with significant payroll gains, increased participation, and rising immigration, is a key driver of this economic vigour.

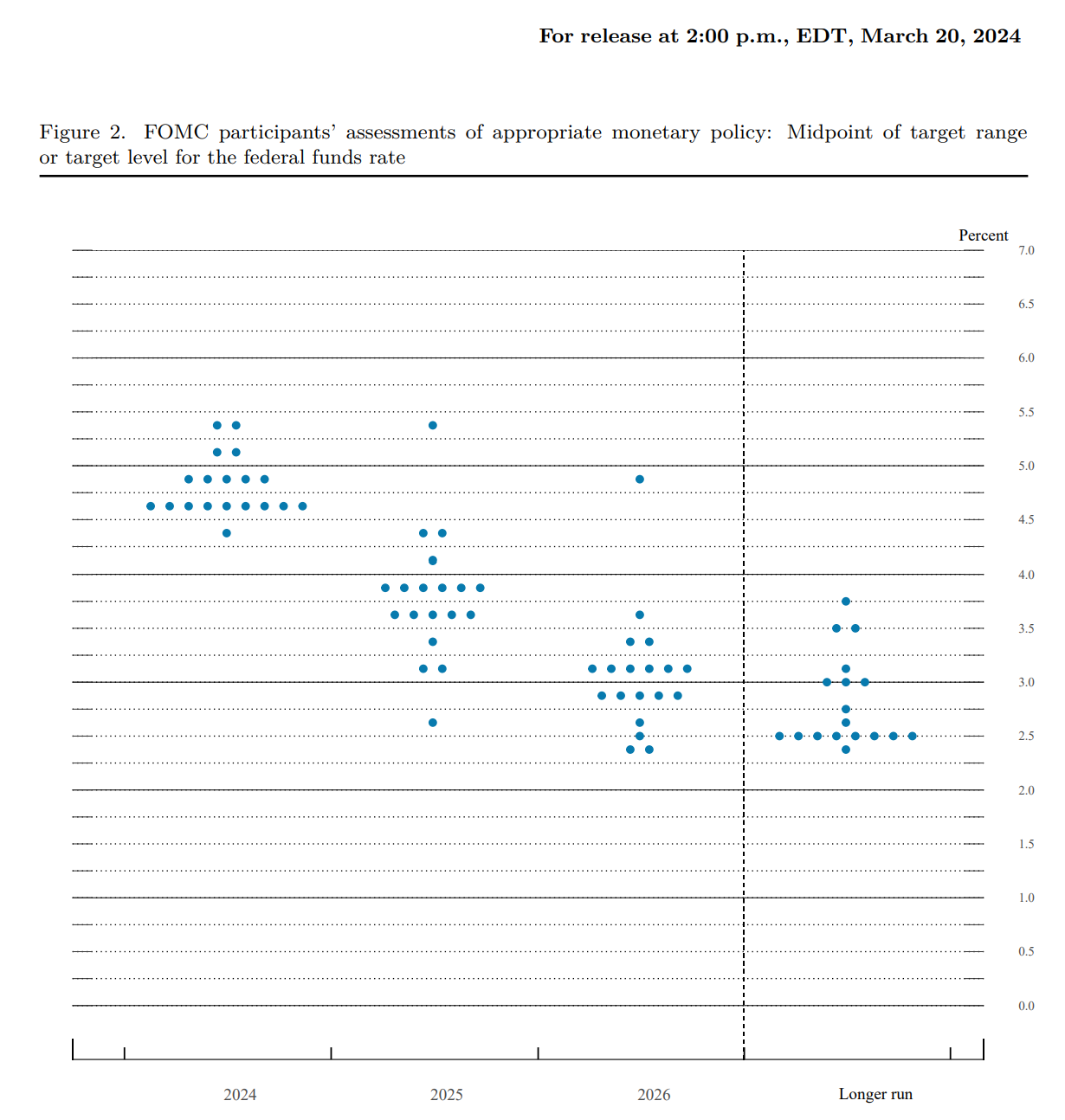

The Federal Open Market Committee's (FOMC) dot plot, released on March 20th, provides valuable insight into the future trajectory of interest rates. This visual representation depicts a gradual downward slope towards a long-run terminal rate of 2.5% (the mode). Notably, compared to the December SEP material, the dot plot shows an upward revision in expected rates across the 2024-2026 horizon. This shift likely reflects a stronger U.S. growth outlook, supported by recent positive GDP data for Q4'23.

Despite this, Chair Powell felt that the committee is still committed to rate cuts this year, undeterred by the stronger economic data in Jan 2024. In the meeting, he suggested that “the policy rate is likely at its peak for this tightening cycle”, and a rate cut is to be expected. It seems that the Fed felt the uptick in inflation in Jan is a result of seasonality and should not undermine the “rate cut” narrative. There are other reasons to embrace the narrative as well.

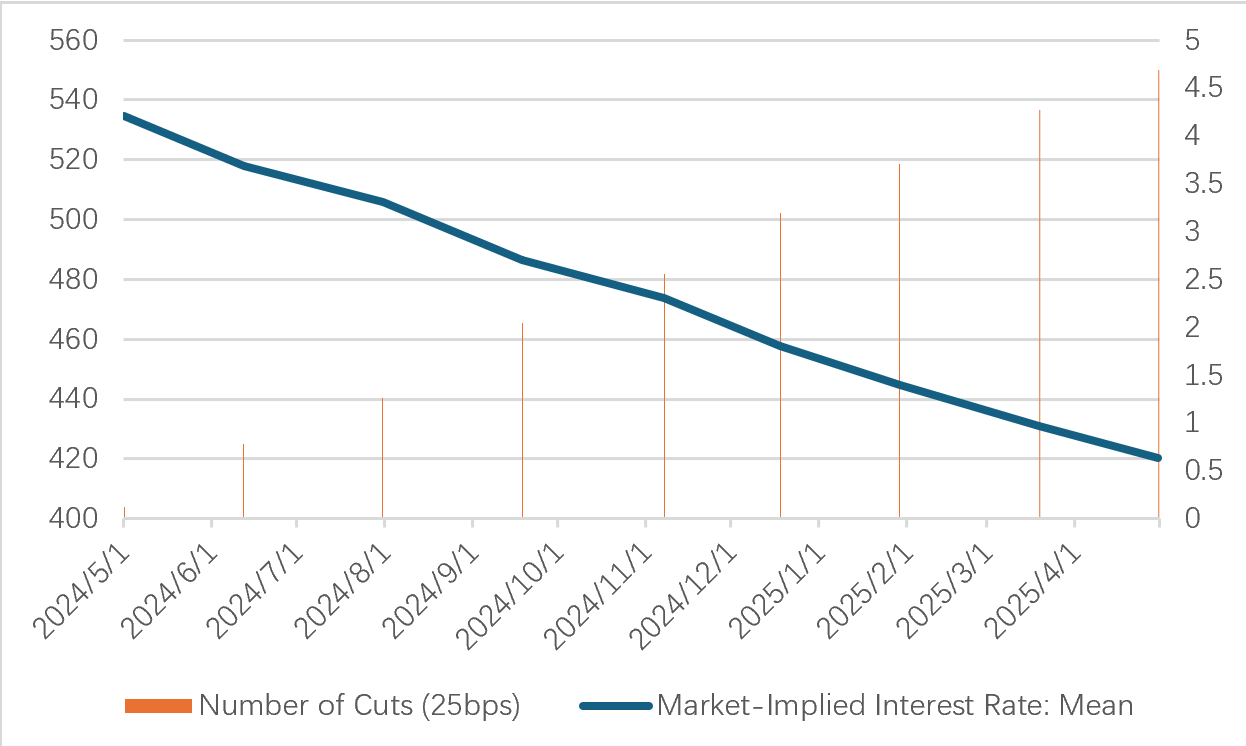

It could be that the current market pricing of interest rates is sufficiently restrictive enough, and any further hawkish comments would tilt the balance too much. We may see this in Figure 6.

Here’s an analogy to understand the market-implied interest rate:

Imagine the market is like a big guessing game about future interest rates. The Fed Watch Tool helps us understand this game by showing the interest rate the market is currently "betting on" based on the prices of things like futures contracts and options. So what we can understand by this is the market's expectations regarding the future path of interest rates based on the current prices of these financial instruments.

CME SOFR (Secured Overnight Financing Rate) pricing data shows that the market prices in 3 cuts by the end of 2024, down from about 5-6 cuts previously expected in January. The readjustment in pricing should give sufficient reasons for the Fed not to worry about the market’s underpricing.

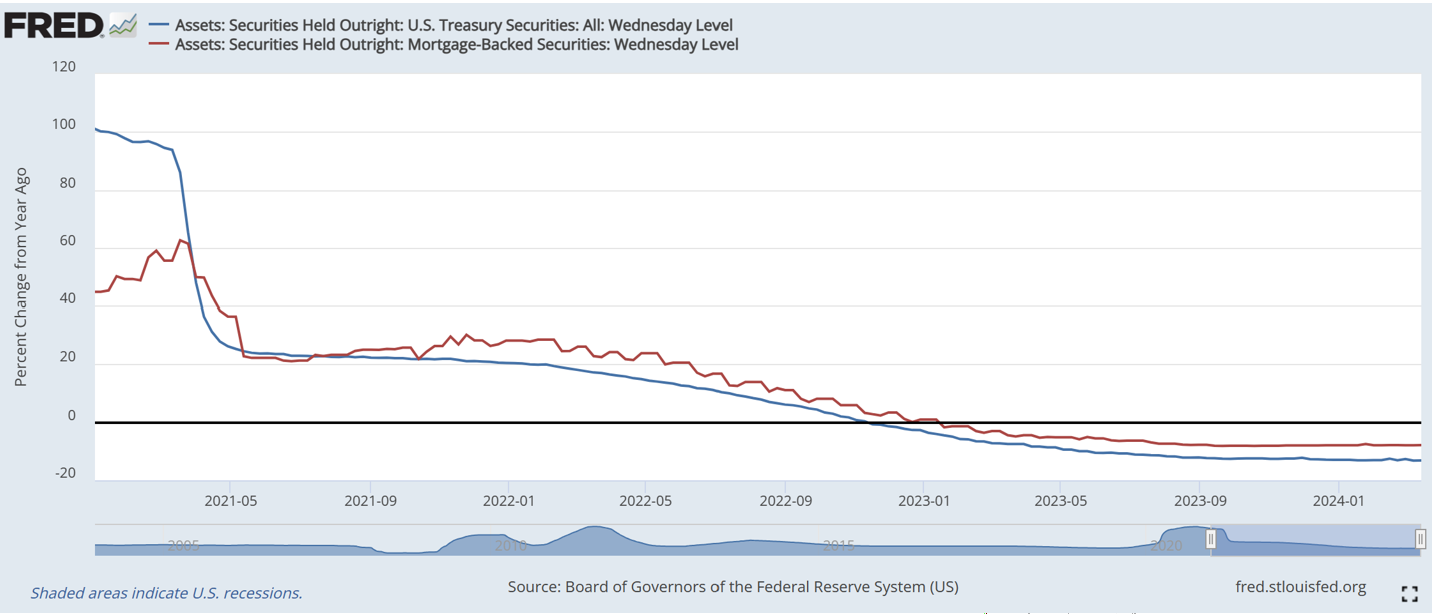

J. Powell also discussed slowing the pace of decline in the securities holdings, “to avoid the stress in money markets”, so going forward the effect of quantitative tightening on the overall liquidity conditions should ease further, adding to the currently bullish narrative of US markets.

Asset Market: Bonds, Equities, FX

US equities and bond markets rallied in unison following the FOMC meeting. Prior to the meeting, expectations for a rate cut were in the near term were high, but concerns about inflation data created uncertainty. The FOMC effectively addressed these concerns, paving the way for a market frenzy.

Looking ahead, this rally has the potential for longevity. A confluence of positive factors is exerting upward pressure on asset prices. Structurally, factors like a higher labour participation rate and increased immigration bode well for the market. Additionally, the cyclical benefit of rate cuts strengthens this bullish outlook.

The dollar index experienced a decline following the FOMC meeting, with only minor corrections observed subsequently. Looking ahead, although additional rate cuts by the Federal Reserve are anticipated, it is crucial to also take into account the policy decisions of other central banks. Should these institutions implement coordinated actions, significant depreciations in the dollar index are unlikely. Furthermore, considering the robust performance of the U.S. economy relative to its global counterparts, the prospects for the dollar remain relatively stable.

Europe: Brittle & Exposed

The week has been relatively peaceful for Europe, as we heard from the ECB earlier this month. For this region, therefore, we will briefly three concerns and headwinds for the economic union.

Here are three sources of potential risks for the EU that we wish to highlight:

First and foremost, geopolitics. In recent months we have seen a tactical shift in war strategy with the use of drone strikes on Russian refineries to disrupt Russia’s main source of financing its war. The problem is that these targeted attacks pose significant upside risks to global oil prices. Europe’s growth is flatlined, Germany’s economy weakening and rates are still at 4.00%. This creates a difficult situation for the ECB, as higher interest rates to combat inflation could further dampen economic growth.

Household Spending: Fading Headwind, But Not Without Lingering Effects

While persistent inflation throughout 2023 is expected to have a fading impact on household real income (disposable income adjusted for inflation), the drag on consumer demand will likely linger through the first half of 2024 (H1) in Europe. This will continue to exert downward pressure on economic growth.

However, there are positive signs. Recent data reveals disinflationary pressures taking hold, with Eurozone CPI reaching 2.6%. This suggests inflation might be nearing its peak, offering some light at the end of the tunnel.

External factors such as Europe’s reliance on global commerce and its interconnectedness to the Chinese growth prospect could further exert negative pressure on key sectors within European economies, namely Germany.

In terms of monetary policy direction, the ECB's key interest rates remain static, underscoring a consistent policy stance. The tapering of the asset purchase program aligns with the planned reduction in market interventions, whereas the PEPP portfolio adjustments reflect a strategic approach to balance sheet normalization. The council's ongoing evaluation of targeted refinancing operations underscores its commitment to a calibrated policy orientation, aiming to secure the inflation target and ensure effective policy transmission.

That brings us to the end of today’s report.

It’s Friday and we’re here talking macro, I wouldn’t have it any other way.

As always, we appreciate your support at MMH Research.

Until next time

Credits:

Jingxuan Niu

U.S & Europe Macro Coverage &