The G4 Review (Pt.1)

Hey all,

It’s a late one, I know.

I missed a report last week Friday so I’ve opened this paid report to the whole community as I wanted to recap all the action we’ve seen from G4 central banks this week and earlier this month.

The Bank of Japan: We analyse the BOJ's recent policy decision, its market implications, and the ongoing challenge posed by the central bank's balance sheet.

The Bank of England: We examine the BOE's decision to maintain interest rates, its alignment with the US Federal Reserve's monetary policy outlook, and market expectations for future rate movements.

BOJ: Out of Negative, For Good.

On March 19th the BOJ ended its 8-year-long negative rate policy along with its Quantitative and Qualitative Monetary Easing (QQE) program. The Bank considered the policy frameworks “fulfilled their roles” as cited in their monetary policy report, the split to hike rates to a range of 0 - 0.1% was a 7-2 majority vote.

Here’s what you need to know:

The Bank will continue to purchase JGBs (an 8-1 majority vote in favour)

The Bank will discontinue purchases of index-linked ETFs and Japan real estate investment trusts (J-REITs).

The bank will gradually reduce the amount of purchases of CP (Commercial Paper) and corporate bonds and will discontinue the purchases in “about one year”.

Whilst the majority, c.58% of Economists surveyed by Bloomberg, expected the policy shift to come in April we at MMH Research were rather optimistic about a March hike given the prospect of a strong Shunto wage negotiation. Rengo, Japan's largest labour union federation, managed to secure a 5.28% wage hike for its union members. This was a blowout vs 2023’s 3.6% wage hike and the expectations for a 4.1% wage hike, this marked the largest increase since 1991.

Market’s Reaction & BOJ Certain Despite Weak Data:

A few hours before the BOJ meeting I checked IG’s client sentiment to see how traders were positioned; of no surprise the majority were short. It was a tempting trade, but as discussed last week, a trade that has become too obvious and too crowded never ends profitably.

In the aftermath of the meeting, the Yen fell 1.51%, to close at 151.00 against the dollar. The lack of signalling further rate hikes weighed on the Yen resulting in both a weaker yen and lower yields on JGBs despite the YCC policy being removed.

The carry trade continues.

Japanese exports have exhibited a robust recovery since December 2023. Following a modest decline of 0.2% in November, exports surged to 9.7% year-on-year growth in December. This positive trend continued in February, driven by a significant 20.1% increase in transport equipment sales. Notably, demand for motor vehicles (up 19.8%) and cars (up 23.8%) within this category displayed strong gains.

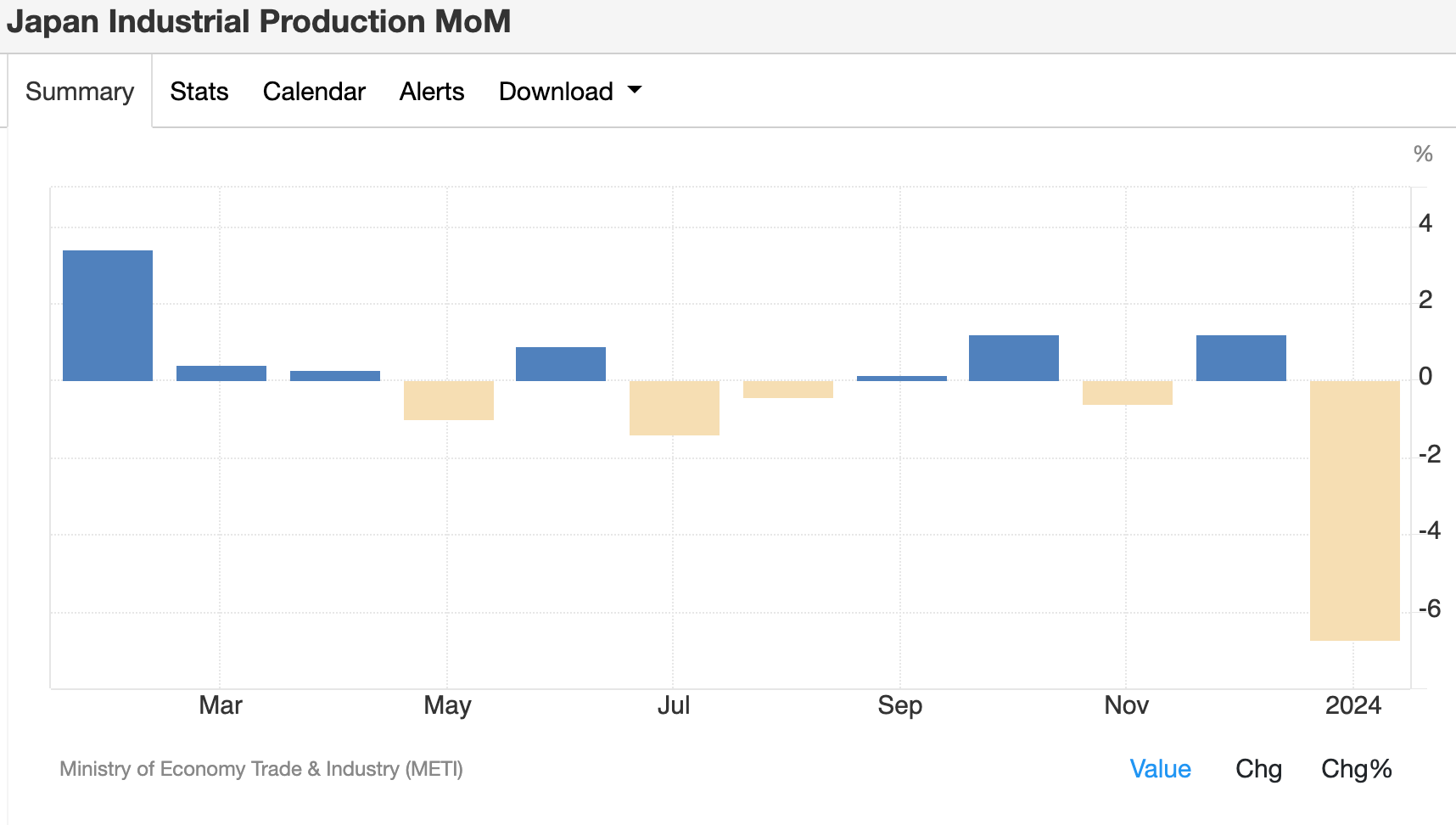

However, when looking elsewhere in the economy the economic data isn’t as optimistic, industrial production has been in a sideways trend over the last 12 months and experienced a large one-month decline in January mainly due to the effects of a suspension of production and shipment at some automakers.

Despite the negative impact of the production suspension on household spending, which declined by 6.3% year-on-year in January, the BOJ's decision to raise rates to 0%-0.1% signifies their overall confidence in the Japanese economy's underlying strength.

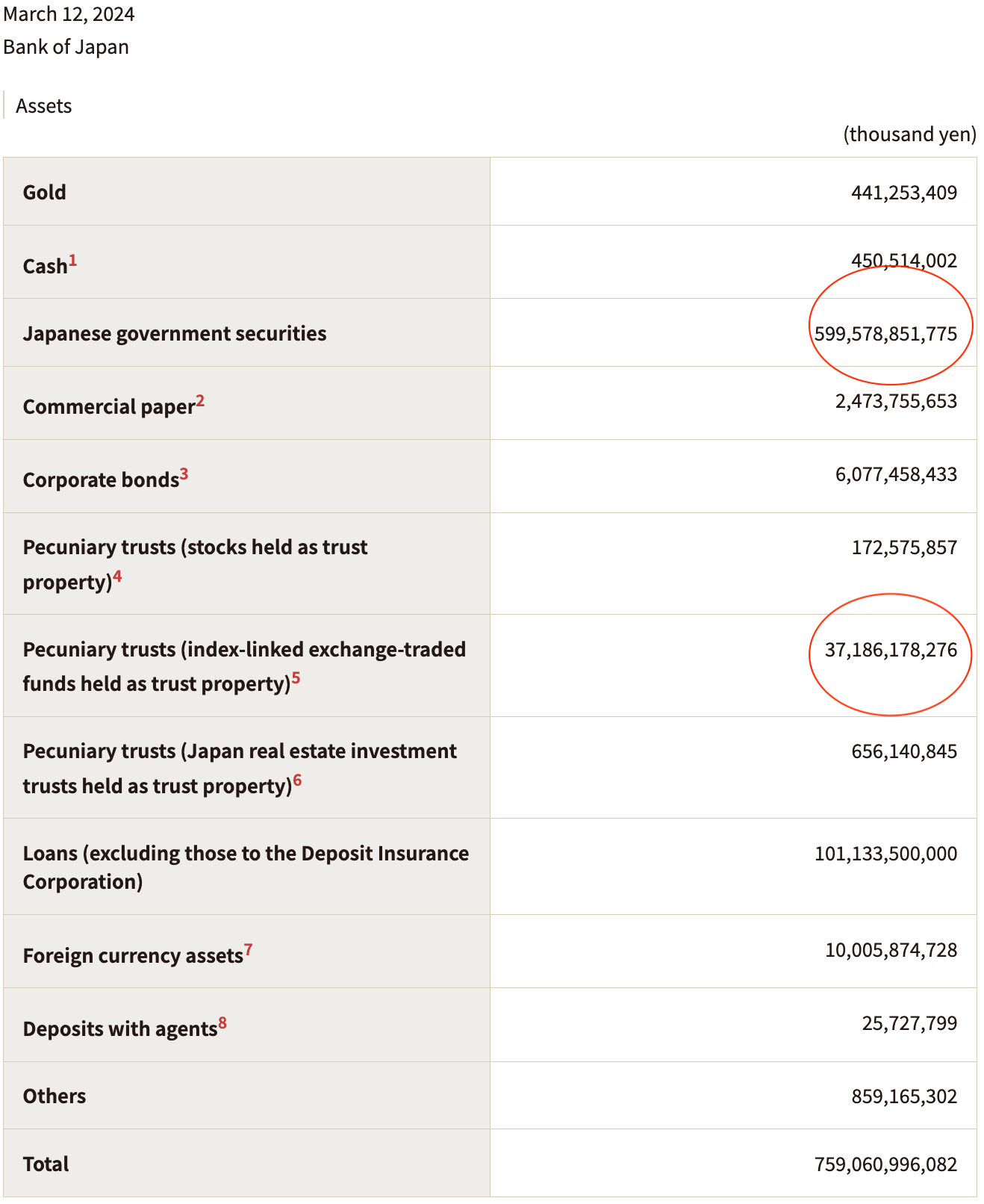

BOJ Balance Sheet

The BOJ's balance sheet, as of March 12, 2024 (Figure 4), reveals a unique feature: holdings of index-linked exchange-traded funds (ETFs). Unlike other major central banks, the BOJ's ETF holdings previously tracked the Nikkei 225 but have since shifted to follow the broader Topix index, which reflects the entire Japanese stock market.

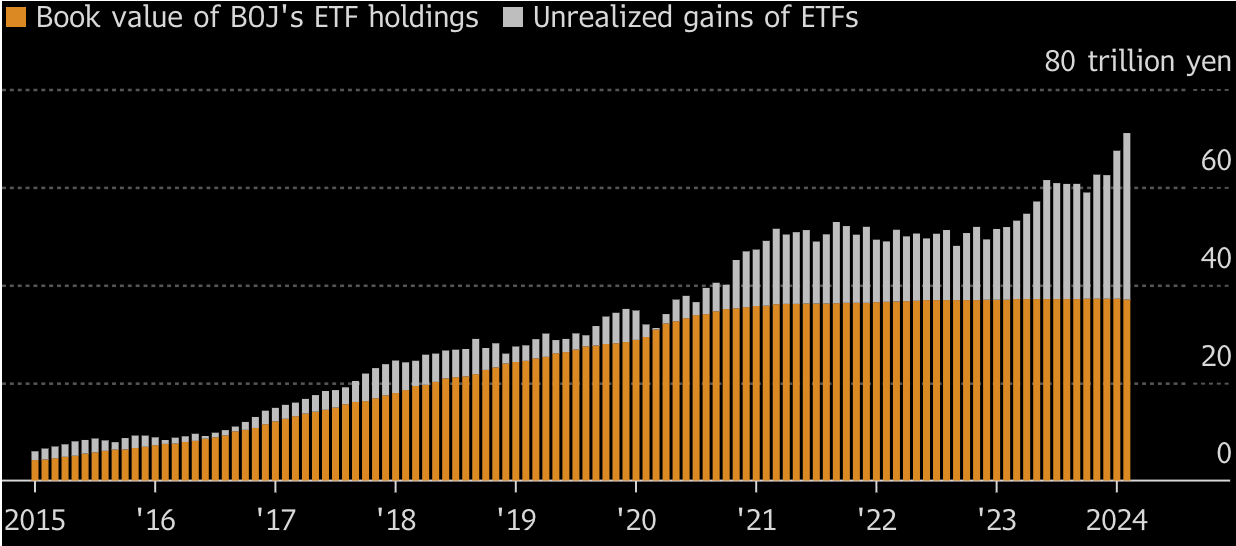

The two most notable assets on the BOJ’s balance sheet have to be JGBs and their index-linked etf purchases. From BOJ’s monetary policy report, we know that they will axe ETF purchases, but bond purchases will continue; the question we have to consider when understanding the path to normalisation for the BOJ is what will they do with their ¥37 trillion ETF holding. This ¥37 trillion as seen on the balance sheet represents the book value of their ETF holding, not the market value, the below figure will put into retrospect the size of the BOJ’s ETF holding.

The total market value of the BOJ’s ETF holding is ¥70 trillion…

Let me put that in perspective, the total size of Japan’s equity market is ¥977 trillion. The BOJ holds the equivalent of 7% of Japan’s equity market. Over the past decade, there have been numerous points of criticism hailed at the BOJ for intervening in its stock market, however, the BOJ does this for two main reasons:

Lower Equity Risk Premium: By having such a strong line of defence in the event of a market downturn the BOJ buys ETFs to promote more risk-taking activity in the overall economy by lowering the perceived risk of investing in equities (risk premium).

Increase Liquidity: Since December 2010 when the BOJ first initiated this program, they have purchased ¥37 trillion worth of ETFs, averaging out ¥2.84 trillion per year. This capital has unequivocally driven up the price of Japanese equities making them increasingly attractive both for domestic and international investment.

You may be thinking that the amount of ETFs the BOJ holds is relatively small compared with JGBs but the key differentiator is that there is no maturity date for ETFs, bonds, however, will mature and naturally roll off the balance sheet meaning the BOJ can either:

Immediately sell-off ETF holdings

Hold onto ETFs and slowly begin to sell off holdings

Never sell

Considering the likelihood of each option: Eliminating ETF holdings from the balance sheet (option 1) carries a very low probability (1%). Such a move would likely trigger significant capital flight from Japanese equities.

Option 2, a gradual reduction in holdings as the BOJ normalises policy, seems more likely (60% probability) assuming continued elevated inflation justifies tightening in liquidity and financial conditions.

However, with the BOJ's history of unconventional policy, option 3 cannot be entirely discounted (remaining 39% probability). This scenario involves the BOJ retaining its holdings indefinitely, benefiting from potential capital appreciation and dividend income from the ETFs.

The Bank of England

Earlier today the BoE met to hold rates at 5.25%, a 16-year high for the Bank.

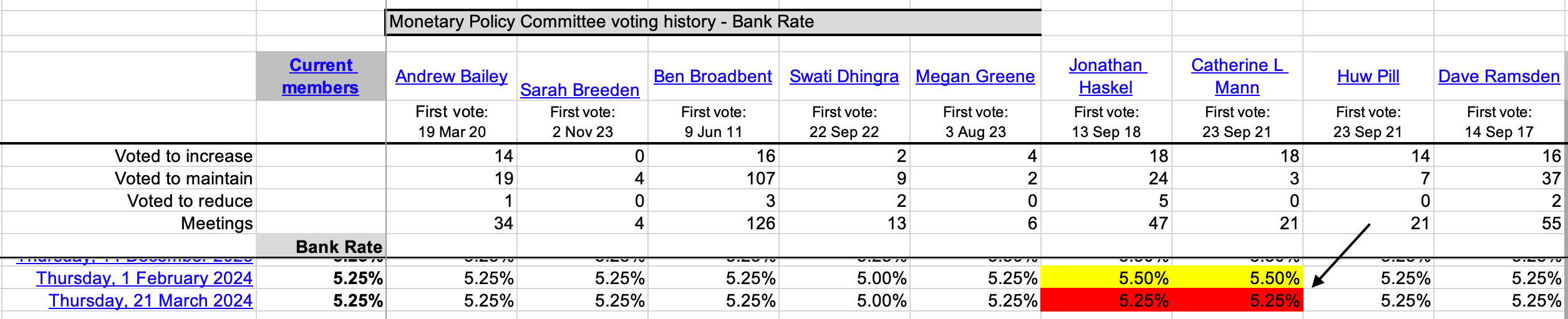

The MPC voted by a majority of 8-1 to maintain the Bank Rate at 5.25%, one member, Swati Dhingra, preferred to reduce the bank rate by 25bps to 5%, but most notably the two hawks Jonathan Haskel and Catherine Mann voted to maintain rates, a dovish tilt from their last vote to hike rates further as seen in Figure 6.

If we look back to February 1st 2024, we can see that both Jonathan Haskel and Catherine Mann voted for a rate hike, whilst all other members voted in favour of holding rates at 5.25%. This shift from two of the most hawkish BoE members signifies the agreement amongst the BoE that financial conditions have been sufficiently restrictive. It’s a data-dependent world for the BoE and Fed with both central banks looking forward to when the first cut will come; expectations have the cut for the BoE and Fed priced for June.

This dovish undertone was largely reflected in the pound’s performance today; sterling slipped 100pips post the release largely due to the BoE’s positive sentiment surrounding inflation as the headline reading sits at 3.4%.

In the monetary policy summary and minutes, the Bank highlighted how in their recent Market Participants Survey, the median respondent expected a median 75bps reduction in the policy rate this year starting in August. They also anticipate the neutral interest rate to be 3.25% for the Bank. These expectations for rate cuts align with the broader market outlook for similar actions by the Federal Reserve in 2024.

As a primer:

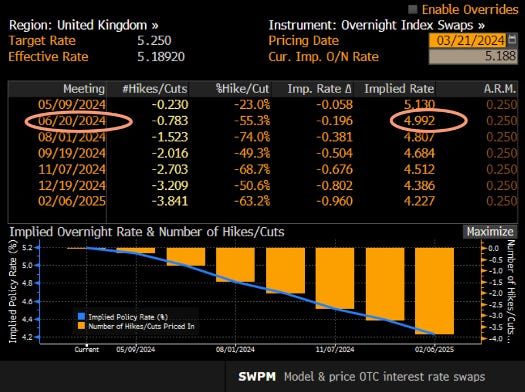

The OIS rate reflects the market's expectations for what the future overnight rate will be at the time the swap matures. It's important to note that the OIS rate is not the actual future rate, but rather the market's best guess, therefore giving us the best probabilistic insight.

Based on the implied o/n (overnight) rate, the market expects cuts to settle around 4.3% at the time of the Bank’s December meeting this year, meaning the policy rate would have had to be cut at least 3 times in 25bps increments to achieve the market’s expectation.

G4 Central Bank Policy Convergence (Excluding BoJ):

A trend towards coordinated monetary policy emerges among G4 central banks, with the exception of the Bank of Japan (BoJ). Most major central banks are now holding off on anticipated rate cuts initially expected for the summer.

UK Economic Challenges:

While specific details on the UK's economic weakness will be covered in a separate report, the country is currently experiencing a mild recession. Macroeconomic headwinds are anticipated, with the primary concern being the health of UK consumers. Rising mortgage rates continue to pose a significant challenge to household financial well-being.

I hope this report provided a clear synopsis of the recent events from the BoJ and BoE. In our next report, we uncover the Fed’s decision and the ECB. We’ll also outline what trade ideas we have been working on to reflect our ever-changing picture of the macro climate.