Currency Plays: Cable Shorts, Yuan Shorts

Currency Plays: Cable Shorts, Yuan Shorts

Capitalising on Weak Yuan and Pound through Targeted Trades Backed by Macro Trends and Data

Hey crew,

Glad to be back.

It’s been a hectic but very fruitful start to the new year.

The macro universe is large in swing, geopolitics driving the headwinds of markets as well.

As I’ve said in previous reports, I want to make my research actionable and truly educational for you all.

So, today I’ll be sharing two key currency plays. The reasons and the macro data behind my cable short idea and my Yuan shorts.

Without further adieu, enjoy:

Bloodbath In Chinese Markets

Positioning: Underweight

Earlier this week I opened a long position on USD/CNH.

For a multitude of reasons, many of which I shared in my last report covering China and its current economic challenges.

To give you a clear and concise view of why I shorted the Chinese Yuan here’s my thought process.

No demand for Chinese assets

Strong capital markets with consistent returns are typically a magnet for foreign investors, attracting them to buy the currency for outsized gains. However, this hasn't been the case for China since 2018, where the Hang Seng Index has declined by over 40%, dampening investor appetite and contributing to the Yuan's depreciation

Since the trade war commenced China’s equity market the Hang Seng Index has declined by more than 40%. China’s crackdown on the public sector during 2021-2023 also contributed heavily to investors withdrawing capital and domestic businesses moving abroad to destinations such as Singapore. Clear capital outflows.

Weak Growth Data & Deflationary Fears Mounting

Although clocking in at 5.2%, Chinese GDP came in lower than analysts expected which escalates concerns that even with all the fiscal aid and support packages China’s economy failed to meet expectations. The question arises, what happens when this unprecedented level of support ends?

The Chinese government are planning to support its domestic equity markets with a $288bn support package amid the large selling seen on the Asian stock index. The prospect of further fiscal spending has sown doubt among both retail and institutional investors, with concerns about its long-term impact on the sentiment around Chinese equities making them hesitant to commit with a long-term perspective.

As discussed in my report last week, China’s deflationary environment presents a unique challenge to the PBOC. Traditional monetary policy tools aren’t working or stimulating markets. This brings me to point no.3.

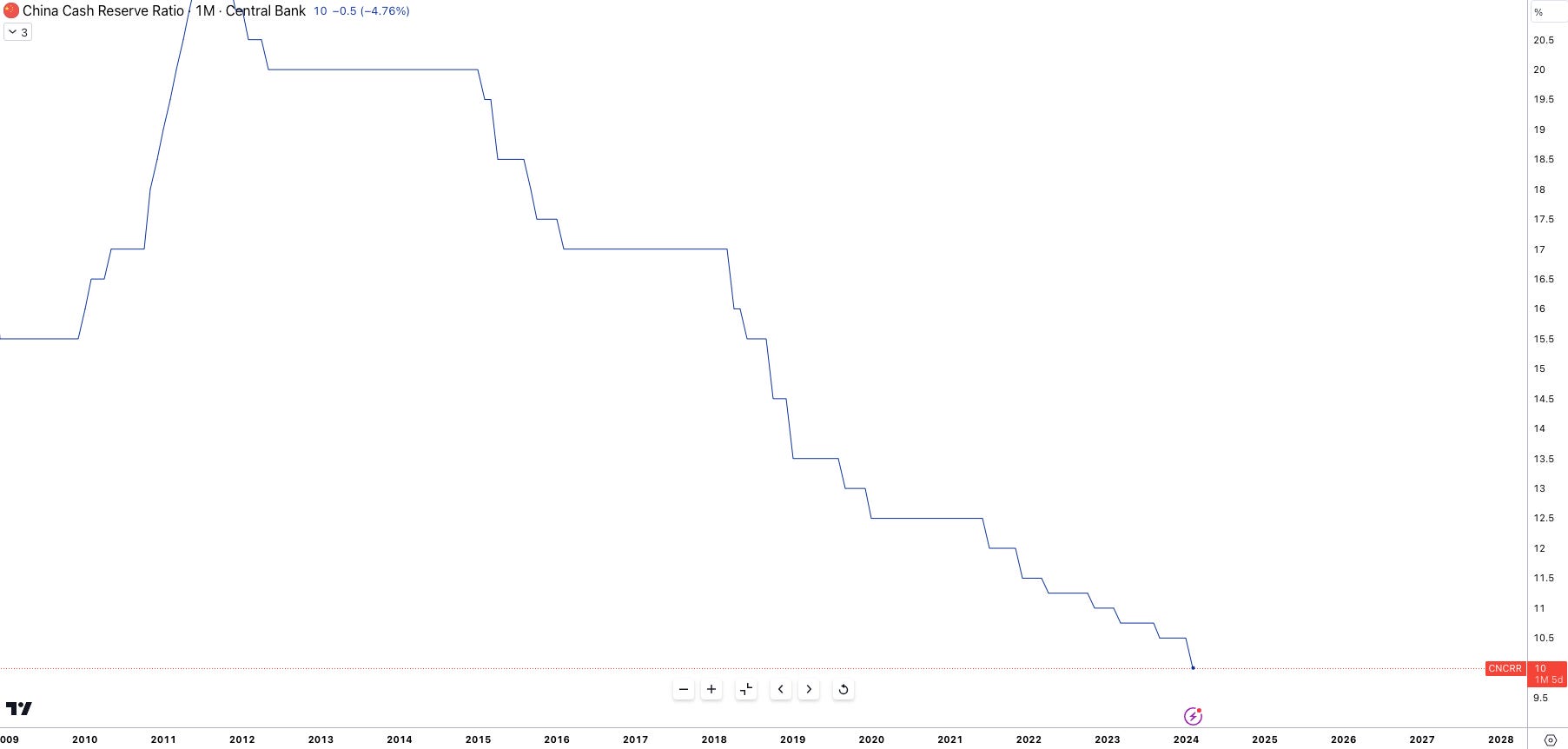

Banks don’t want to lend

Yesterday, the PBOC’s governor Pan Gongsheng told reporters they will cut the RRR (reserve requirement ratio) for banks on February 5th by 50bps. The RRR determines the amount of cash banks have to keep in reserve for liquidity purposes. Now what’s unusual about this is the size of the RRR cut.

Over the past two 2 years, the PBOC has cut the RRR only 25bps at a time, however, this 50bps cut emphasises the importance of stimulating the economy. The unfortunate fact is that even with the reserve ratio lowered, practically freeing up ¥1 trillion, banks are unwilling to extend credit through the financial system further clogging up the flow of credit due to weak consumer consumption and demand.

Geopolitical risks

The increasingly complex geopolitical landscape, particularly centred around China, presents significant challenges for investors. Firstly, China's strategic rebalancing and stated ambitions towards Taiwan unification have elevated tensions in the region. Any military intervention in or around Taiwan by China would likely trigger significant responses from the United States and its allies, potentially disrupting global trade and financial markets. Secondly, the upcoming US presidential election adds another layer of uncertainty.