Currencies: A Global Macro Primer

The Unsung Heroes of Global Macro, FX.

Hey crew,

A macro report on Monday?

Yes and no.

This primer was meant to be sent last week Thursday but I’ve been recovering from food poisoning since Thursday morning. Wasn’t pretty I can tell you that.

Anyway, I thought I would open this report to all subscribers, a helpful deep primer on currencies.

You might want to open this report on the web.

Without further adieu, enjoy.

Macro Snapshot

Politics & Currencies

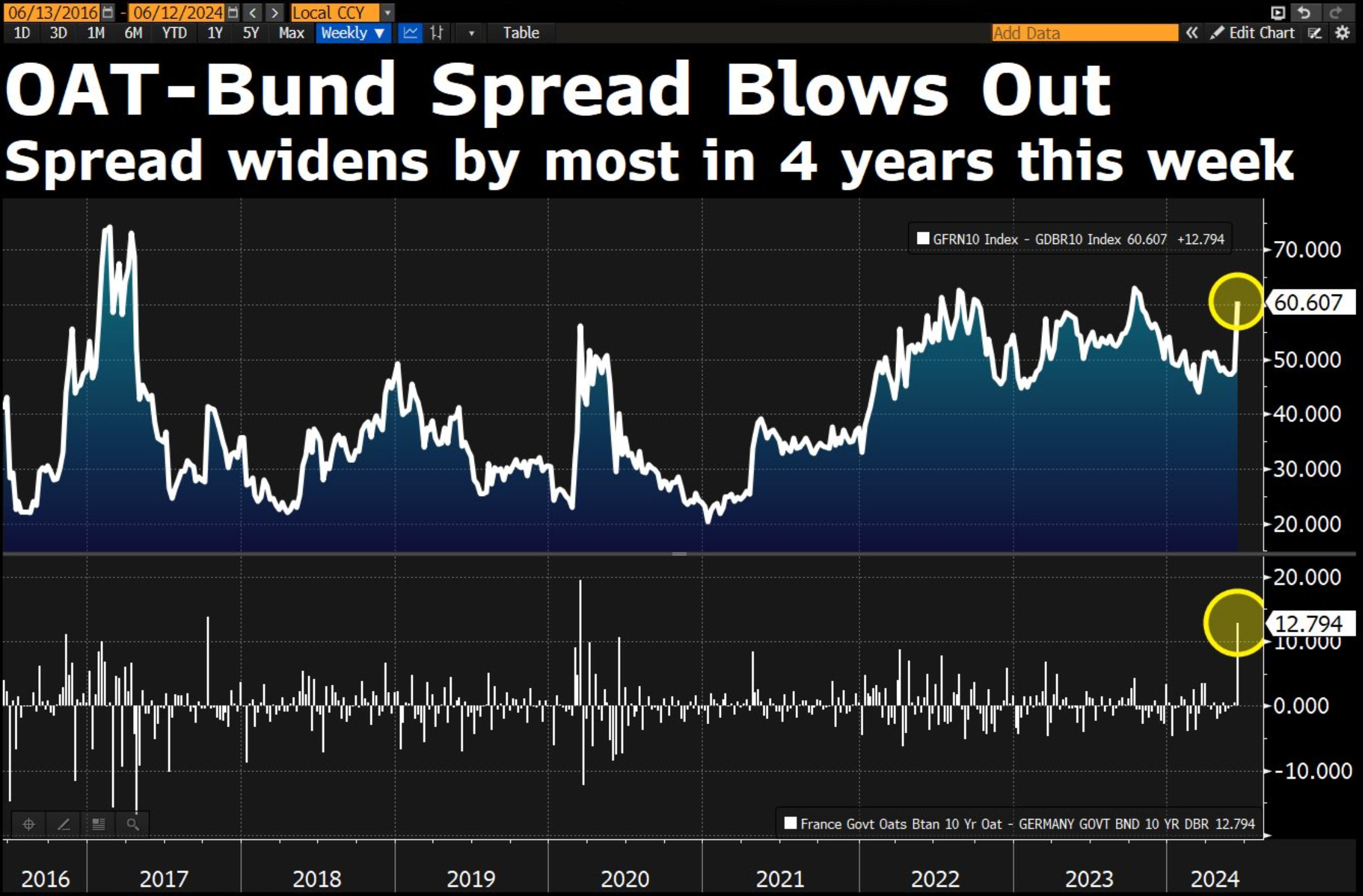

If you’ve been watching rates you would've noticed some sharp movements across the Euro and French OAT bonds. On Sunday night President Macron called a surprise snap election which spooked markets, triggering the Euro to gap lower on the Asian open and widening the OAT - Bund spread to 4-year highs.

The past two weeks have been a prime example of how political instability causes unwanted vol across all asset markets, equities, FX & yields.

Without diving into Europe's political mess, here’s a simple explanation of what’s going on.

Macron is the leader of the Renaissance centrist party, who has been in power since 2017. However, in the recent European Parliamentary elections last week his far-right opposition, Marine Le Pen of the National Rally party, secured approximately 31% of votes whilst Macron’s party only managed 15%. Macron was pretty much blown out of the water.

The significance is that losing in the way Macron did suggests a shift in the political landscape which will challenge Macron’s policies. So, instead of waiting until 2027 for the next National Assembly elections in France, Macron scheduled them for June 30th and July 7th to try to secure the lower house of the government.

Can say goodbye to stability in Europe for a while.

The weakness in the Euro is evident when observing the performance of a basket of EM/DM currencies against the Euro. The Euro has weakened as much as 2.5% against the basket of currencies just last week alone. No such thing as good vol when politics is steering the wheel.

Dots of the Week

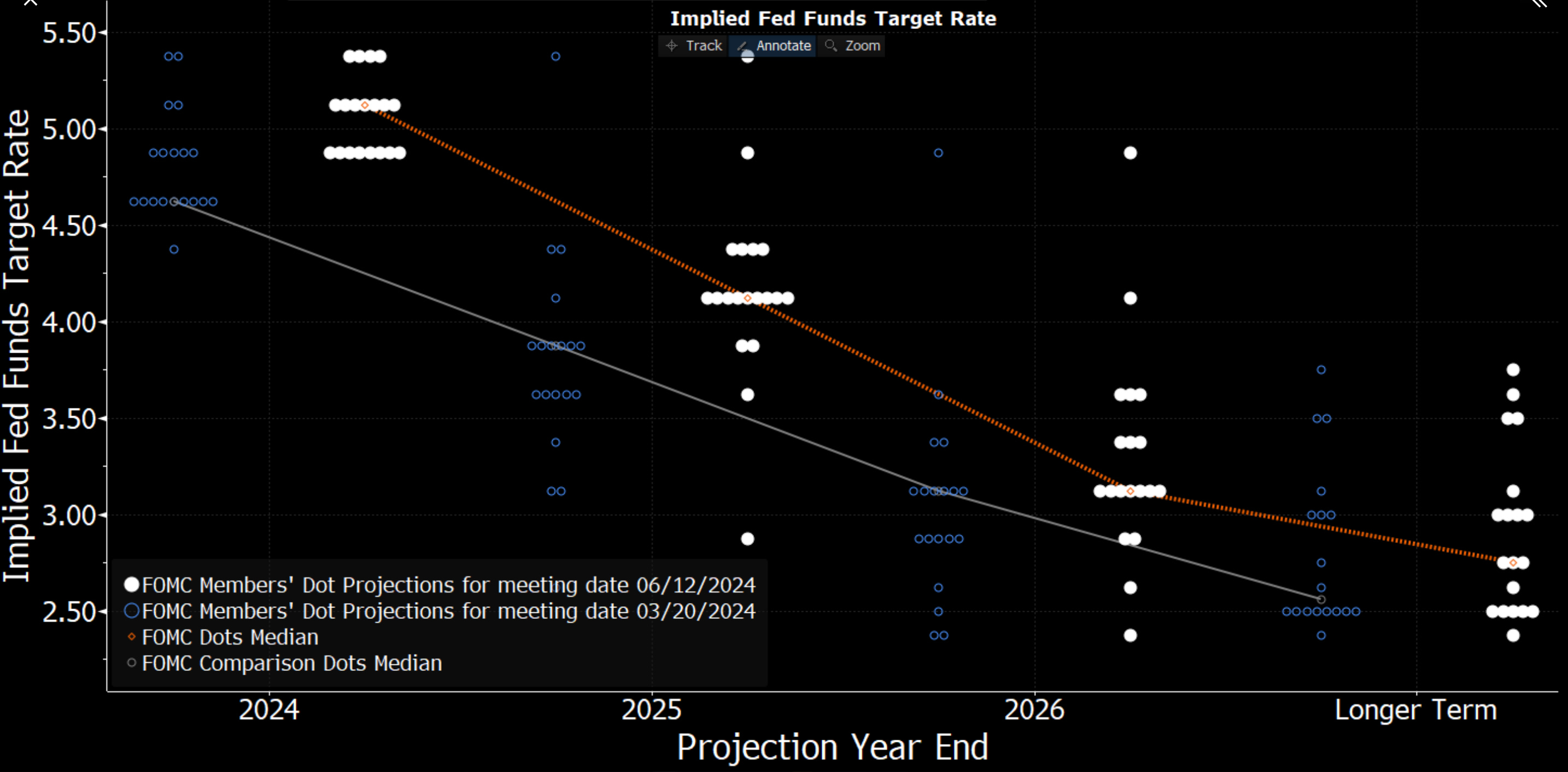

Without wasting a whole report on the FOMC meeting here’s the main event recap.

There was a notable shift higher in the FOMC’s dots. Compared to March where the FOMC was projecting 75bps of cuts (blue dots) for the year vs June’s dots where 7 members only see on 25bps rate cut this year whilst 8 members still hold onto the consensus 2 cuts for 2024.

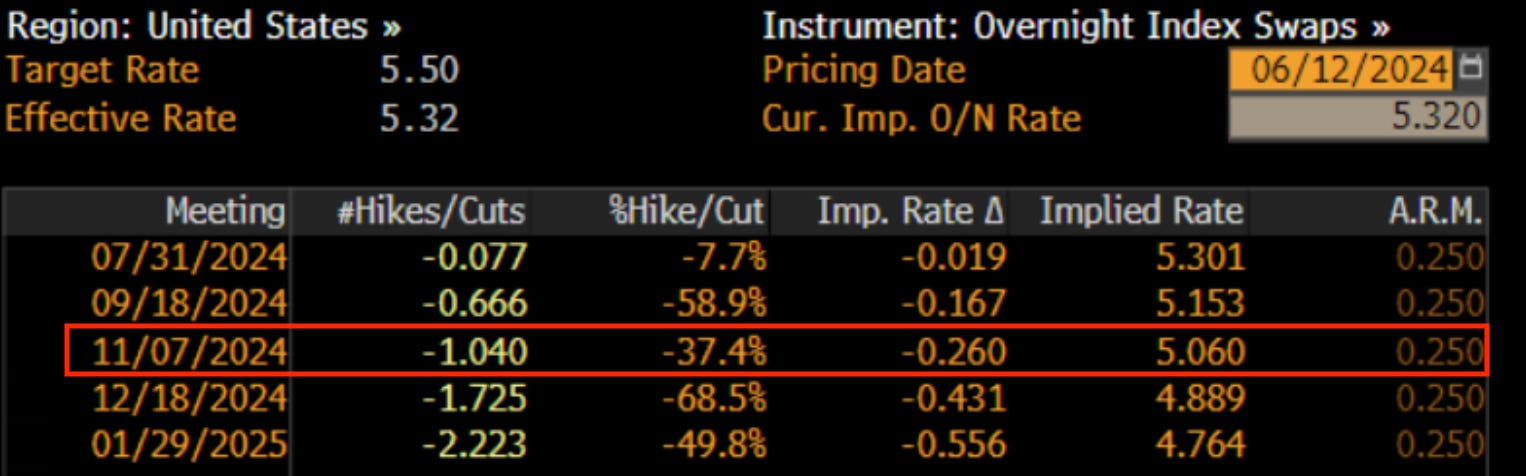

The OIS curve is fully pricing in the first rate cut in November, with the potential second cut coming in December. However, markets still need slightly more convincing to put more weight behind a December cut.

Chart of the Week

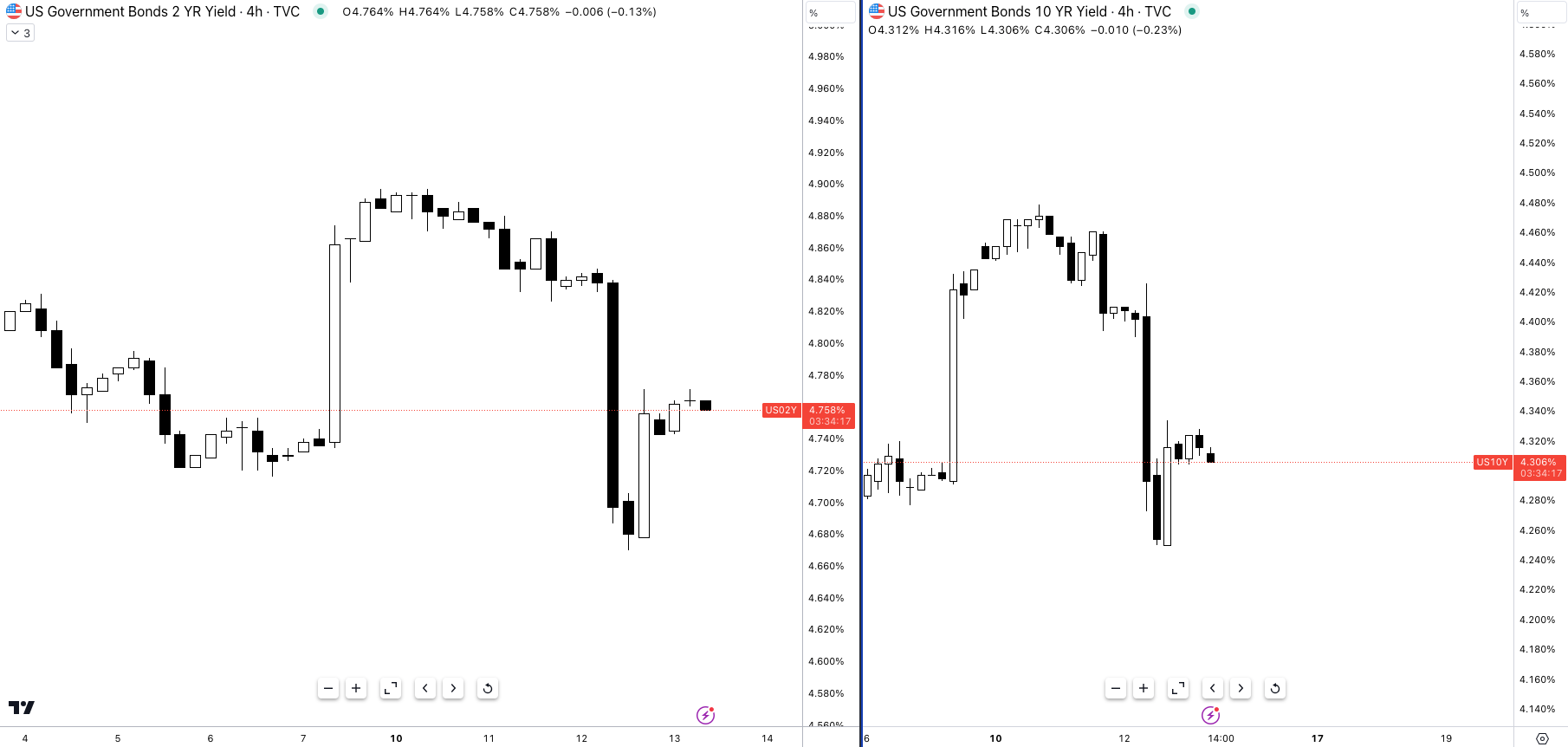

It would have been near impossible to neglect this chart here after last week’s US CPI figure surprising to the downside.

Inflation in the US slowed to 3.3% vs 3.4% consensus and core inflation slowed to 3.4%, down from 3.6% and below the 3.5% consensus.

Despite the hawkish dot plot released during the FOMC meeting, the markets seemed unwilling to give back gains made from the CPI move earlier in the day.

Currencies. The Pillar of Global Macro.

Currencies matter. Probably one of the most sensitive markets to changes and adjustments in interest rates, geopolitics and fiscal policy.

As explained over the last two reports, we have three prime examples of currency sensitivity, the MXN, EUR and the INR. All three currencies have been subject to politically instilled volatility, something which is impossible to profitably navigate until the cat’s out of the bag.

Just take a look at the spot return for the MXN since the end of May, -8%.

For the most part, and I mean roughly 90%, the main drivers of currency markets are interest rate differentials and implied future policy rates. I’ve touched on this countless times before, yet whilst it may be common knowledge many people still fail to capitalise on the opportunities presented by the world of rate differentials.

History will tell us that there’s more to currency movements than just FX, which is true, but that mainly applies to the EM basket of currencies. During my brief stint working at a research house focused on EM sovereign debt, I was exposed to numerous examples of currency crises stemming from sovereign defaults.

The infamous Tequila Crisis of 1994 provides a clear example of how economic and political factors can intertwine to create market turmoil. In the early 1990s, the Mexican government attempted to combat inflation by raising interest rates. However, this strategy also led to slower economic growth. This precarious situation was further exacerbated by the assassination of a leading presidential candidate, triggering a wave of capital flight.

As a result, the Banco de Mexico devalued the Peso against the dollar, the only issue is this act fired back in more ways than you could imagine. The devaluation sent Mexico’s risk premium yield through the roof as investors’ concerns about paying its sovereign debt became prominent.

Fear spread through neighbouring LATAM countries causing an exodus of capital from LATAM countries which sent the Peso lower by c.120%…

Whilst sovereign crises like Mexico’s 1994 are less frequent they still appear in every macro cycle, take 2020 for example which brought extreme levels of vol to LATAM currencies. As a whole, portfolio outflows reached $83.3 billion in March ‘20. This practically reversed the profitable carry that had been prevalent since early 2017.

Going back to the GFC days, before the ‘07 crises began you had the $82.2 billion Argentinian default. They missed a debt payment in Jan ‘02 and had to restructure a distressed debt offering where bondholders received a haircut of c.70% on the bond’s face value. As you would expect, the contagion effect was significant, with weakness across the BRL, MXN, COP & other LATAM currencies.

Even if you’re solely focused on equities, knowing and understanding the fundamentals of FX is non-negotiable. This is where we move into the universe of currency heading for portfolio returns and volatility reduction.

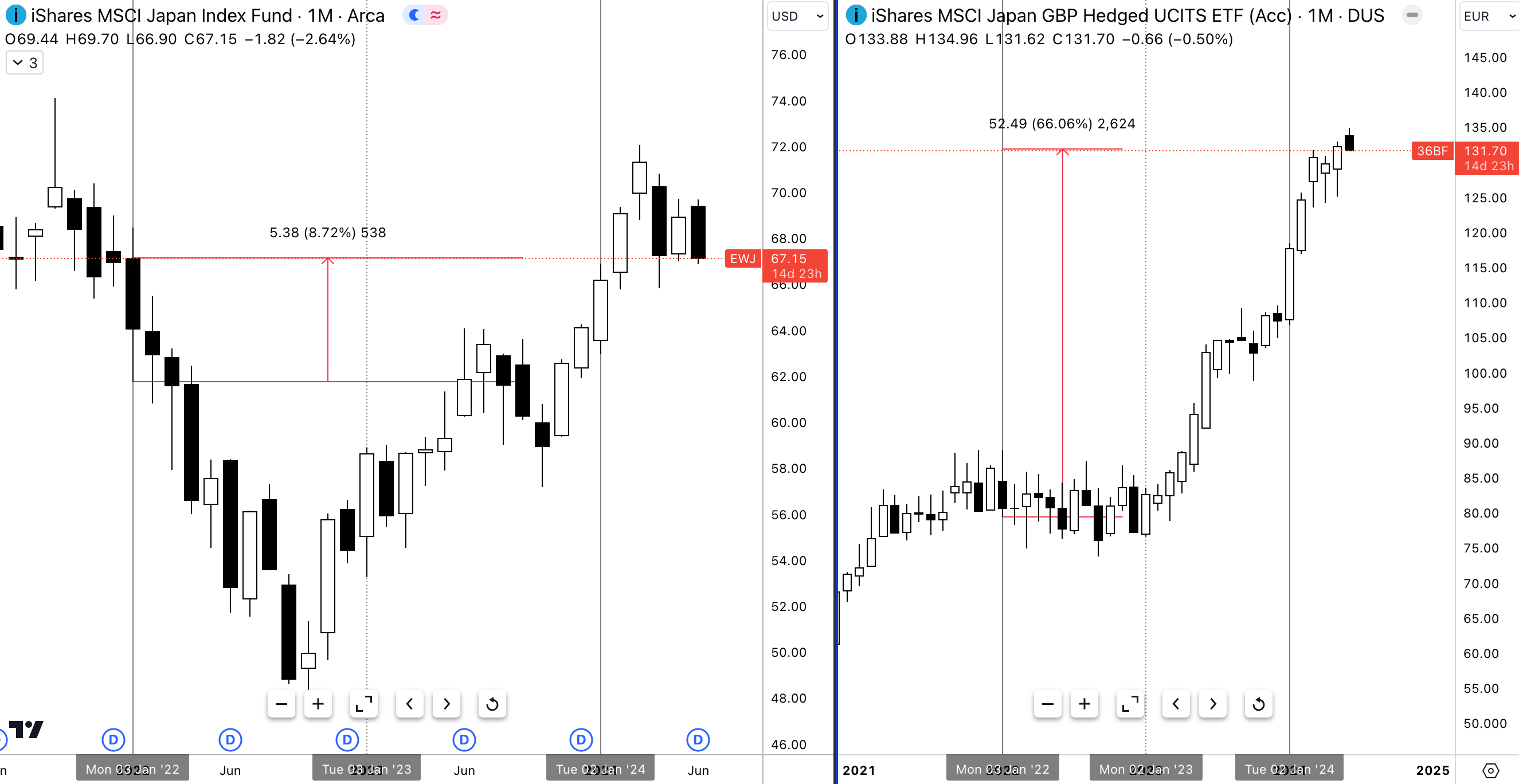

Long Japanese equities was an idea I was exploring at the very start of the year, but realising I was very, and I mean very late to the party I was happy to wait on the sideline. Since 2022 an unhedged Japanese equity ETF would have returned you roughly 5% ex-dividends, whilst a GBP-hedged Japanese equity ETF would have returned 66% in the same period.

61% over two years, with the large majority of that gain coming in just one year!

P.S. YTD it’s up 20%.

For the simple reason of the pound strengthening against the yen you’ve now created a diversified stream of alpha to your portfolio, just by understanding the future implied policy rates for both central banks, which I must say, isn’t that hard given the BOJ’s monetary policy style.

Step one:

Carefully consider the anticipated monetary policy stance of the central bank in the country where you're investing.

Step two:

Determine the appropriate currency play (i.e do we purchase GBP-hedged JPY ETFs, do we purchase GBP-hedged S&P 500 etf)

Step three:

Make the play.

If I were to knuckle it down to the three most important steps, that would be it.

Automatically your mind should naturally shift to thinking.

What other ETF plays were there that could have been made with this knowledge of rate differentials driving returns?

Your mind may swing instantaneously to Turkey’s MSCI equity index which returned over 100% in nominal terms during 2022. However, the one thing you have to remember is that this was in local currency (Turkish Lira) meaning that the inflation component was not factored in. So, whilst you may hear that certain foreign market returns are attractive, remember the inflation component can easily make those 100% gains look average, which for Turkey was the case as inflation averaged 72%.

The Carry

For the past three years, the carry trade has been one of the most popular, profitable and consistent trades to make. I’ve found myself falling in love with Asian currency markets because of the carry aspect, namely the Yen & offshore Yuan- what a currency to carry right?

The fundamental mechanics of the carry involves a trader borrowing in a low-yielding currency (JPY) and converting that JPY to a high-yielding currency, say the BRL (Brazillian Real) and investing in a high-yielding short-term security.

The example here would be as close to perfect as you could imagine. Take the 2y note in Japan which yields 32bps, now for the same maturity I could yield 11.4% in Brazillian 2y note.

Carry brings to life interest rate differentials, as simple as that.

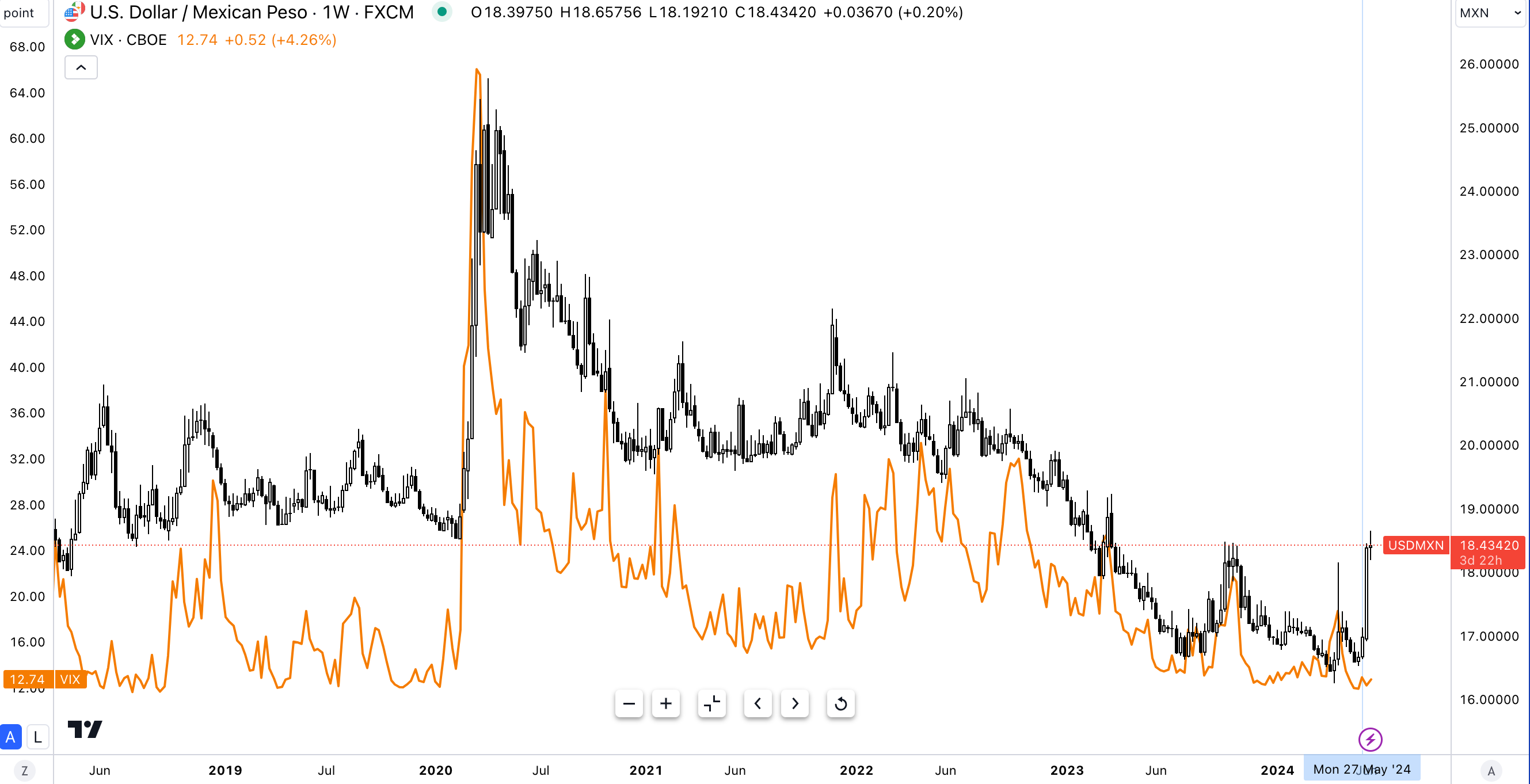

Now what most people fail to realise is the risks involved with carry trades (we’ll speak mainly about LATAM ccy since they tend to have the highest rates).

Carry hates vol.

When you are long carry, you are outright short volatility in markets. It’s visible in the chart above. Whenever there are moments of heightened fear/vol in markets the carry trade is the first position to unwind, and unwind ugly. Take the outbreak of COVID-19 which was pretty much overnight, if you were long carry you would have experienced a sharp drawdown or even margin call on this position.

Once again, just look at the past two weeks in macro, Indian and Mexican elections causing vol = heavy unwind of the carry.

My point visualised.

So we instantly group the (target) carry currencies into the high beta pocket of currencies.

Prior to the Mexican elections, the Peso was up c.2% against the Dollar YTD.

If I sound like a broken record then good, it means I’m getting my point across.

So as a rule of thumb, high vol leads to USD demand so we short high beta currencies. Hence why right now, despite the interest rate differential between the Yen and Mexican Peso, due to elevated volatility you would much rather be long the Yen than the Peso since the Yen is a low beta currency.

Now whilst that sounds right, and in theory, technically it is, there’s a caveat you have to account for.

Fading the carry means you’re now negative carry. So even though volatility may be high, resulting in you going long low beta/short high beta ccy, financing the position would cause you to bleed carry resulting in you eventually liquidating the position.

So, what is the best FX position to be in during high volatility periods?

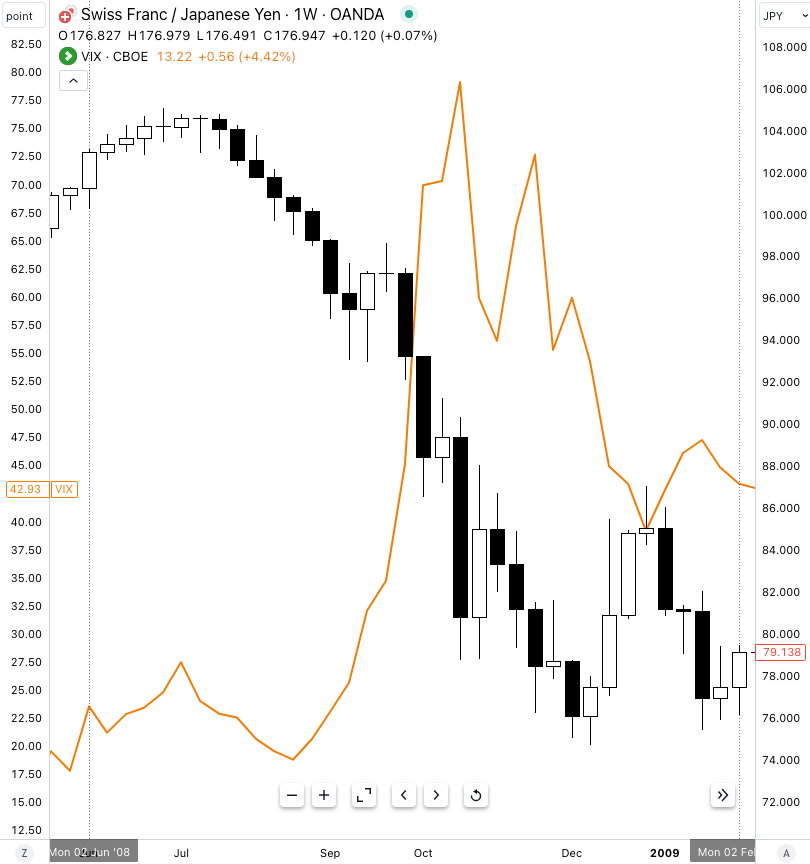

Low negative carry volatility plays:

Short CHF/JPY

Short EUR/JPY

While USD/JPY could be a tempting inclusion due to the recent rise in US-China tensions surrounding Taiwan, the significant interest rate differential between the two countries makes it a risky proposition. For a short USD/JPY position to be profitable, a substantial escalation in trade tensions would be necessary, which could lead to losses if such an event doesn't materialise.

This perfectly depicts how fading the carry would be profitable in periods of high vol while absorbing minimal bleed from overnight rollover fees.

Furthermore, this is a weekly time frame, so you can imagine the ease of going with the trend as volatility remains heightened.

The second position on EUR/JPY looks like this:

Vol spike = Fade the carry

Now it’s not just a huge recession where such opportunities present themselves.

In 2011, the VIX spiked to 31.66, as rumours of US credit rating being downgraded began to grow— after weeks of inaction, Congress missed the August 2nd deadline to raise the US debt ceiling resulting in the triple A rating in U.S credit being downgraded on August 5th by Fitch.

Result? Safety flows to low beta currencies.

Shortly after, and I mean shortly, on August 10th 2011 more crap hit the fan.

Word got out of a French sovereign debt downgrade sparking a huge selloff in equities, particularly among French banks BNP Paribas, SocGen, and Crédit Agricole. The concern stemmed from too large exposure to Greek debt within the French banking system, which of course became a contagion risk affecting the US banking sector as well.

There’s countless events I could talk about, but I believe I’ve gotten my point across, there’s many catalysts that can affect the performance and direction of FX markets. So going forward keep your eyes out for all opportunities because they’re there!

I hope you took away a thing or two.

This was a deeper dive yet (hopefully) still simple to comprehend.

Will be back with you guys this week

If you enjoyed this, do me a favour and send it to a friend— it helps a lot ;)

Great report!

Question, why would we want to short CHF / JPY during a period of high volatility? I was under the impression that it was a low volatility currency, or is it because the JPYs is a very low beta currency??

another perspective on carry with the VIX introduction, thanks Joe!