Beyond The Rates: A Deeper Look At Macroeconomic Influences On FX

Beyond The Rates: A Deeper Look At Macroeconomic Influences On FX

Delving into the Macroeconomic Drivers of Foreign Exchange Rates

Hey guys,

Always good to be back.

NFP data showed relatively mixed labour data, which will provide Jay Powell with some relief based on his recent dovish mantra at the Congressional hearing earlier this week.

Instead of covering the NFP & Fed Congressional hearing today, I thought I would do an in-depth report for you guys next week, after we have received an important CPI print, coming out on Tuesday 12th, just 7 days before the FOMC meeting. So, be on the look out for that.

As for now, enjoy this report written by our research team, headed by Alfie.

Reserve Requirements

Reserve requirements are a tool employed by central banks within their broader monetary policy framework to influence the money supply. This mechanism is typically used to either stimulate economic activity during periods of slow growth or to combat inflationary pressures when the economy is overheating.

Central bank reserves, also known as bank money, are deposits held by commercial banks at the central bank. These reserves serve as liquidity for interbank transactions and do not directly circulate within the real economy. Reserve requirements, a regulatory instrument employed by central banks, stipulate the minimum proportion of total deposits that commercial banks must maintain as reserves at the central bank. This ratio is typically expressed as a percentage.

Reserve requirements are primarily motivated by the need to ensure bank liquidity in the event of depositor withdrawals. This can occur during periods of financial stress, when rumours of a bank's insolvency or concerns about the broader economic climate may trigger a bank run, where a large number of depositors attempt to withdraw their funds simultaneously.

One might question why the level of depositor withdrawals should be a concern for banks, given that they hold our deposited funds.

This concern arises because fractional-reserve banking allows banks to lend out a portion of deposited funds. Consequently, they may not hold sufficient liquid assets to immediately meet all withdrawal requests in the event of a bank run.

Fractional-reserve banking is a cornerstone of the modern financial system. In this system, banks leverage customer deposits by extending loans and credit. For instance, if the reserve requirement is 10%, a bank can legally lend out 90% of deposited funds while holding the remaining 10% as reserves. This practice allows for credit creation and stimulates economic activity. However, it also introduces the potential for bank runs. Let's illustrate this concept with a basic scenario...

Consider a scenario where a bank receives £100 million in total deposits on a given day. Under a 10% reserve requirement, the bank would be authorized to lend out £90 million, leaving only £10 million in liquid reserves. If, on a subsequent day, all depositors demanded immediate withdrawal of their funds, the bank would face a significant liquidity shortfall, potentially leading to insolvency (inability to meet its financial obligations).

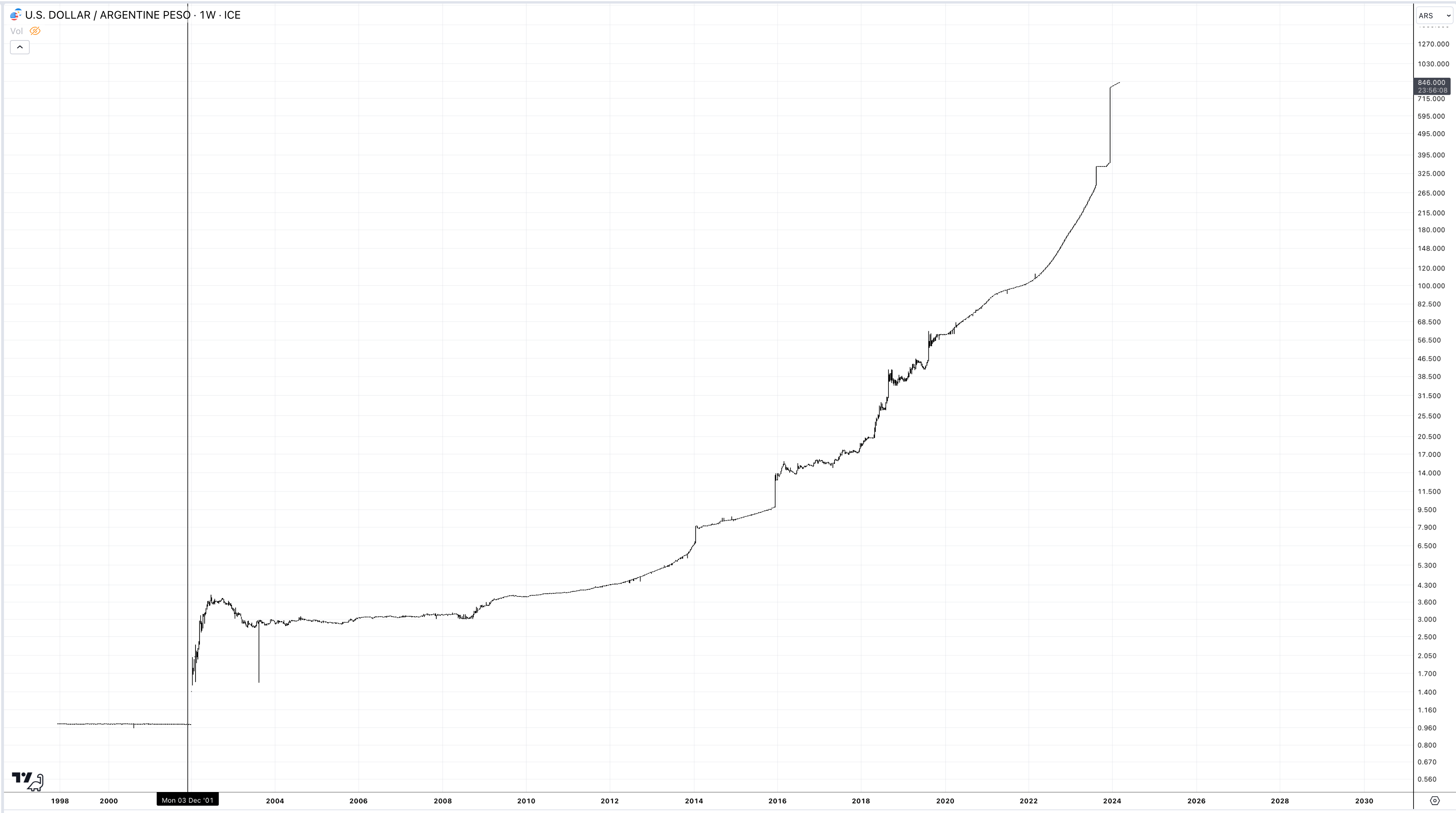

The Argentine economic crisis of 2001 serves as a cautionary tale regarding the importance of reserve requirements and the vulnerability of economies to bank runs. Argentina's situation was characterised by a confluence of factors, including a widening fiscal deficit, mounting public debt, and a fixed exchange rate system that pegged the Argentine peso to the U.S. dollar. This currency peg, often viewed as a vulnerability due to its restriction on monetary policy independence (particularly regarding interest rate adjustments), eroded confidence in the Argentine peso. As a result, depositors increasingly began to convert their pesos to U.S. dollars, further pressuring the currency peg and ultimately triggering a bank run.

By December 2001, following a series of unsuccessful attempts to stabilise the Argentine economy, public trust in the banking system had significantly eroded. Depositors, fearing devaluation of the peso and potential limitations on future withdrawals, engaged in a large-scale bank run. This liquidity crisis forced the government to implement a series of emergency measures, collectively known as the "Corralito." These measures included restrictions on daily cash withdrawals and limitations on the free movement of U.S. dollars. Unfortunately, the bank run ultimately rendered many financial institutions insolvent.

The ramifications extended far beyond bank failures. The crisis spiralled into hyperinflation, a phenomenon marked by a rapid devaluation of the peso's purchasing power, often exceeding 50% per month. This severe inflation, coupled with widespread unemployment, triggered significant social and political unrest. Civil unrest, including clashes between civilians and law enforcement, manifested throughout the country as the economic turmoil intensified.

Now back to reserve requirements.

Reserve requirements also serve as a tool for central banks to influence the money supply and manage economic activity. In a high reserve requirement environment, designed to combat inflation, banks are obligated to hold a larger portion of deposits as reserves at the central bank. This effectively restricts the amount of funds available for lending, thereby limiting the money supply within the economy.

This credit contraction has a two-fold effect. Firstly, banks may raise interest rates on loans to compensate for the reduced lending capacity. Higher borrowing costs often discourage loan applications from consumers and businesses, further dampening economic activity. Secondly, with a tighter credit environment, banks may impose stricter lending criteria, making it more challenging for some borrowers to qualify for loans.

In conclusion, a central bank implements a higher reserve requirement as part of a restrictive monetary policy to curb inflation by controlling the money supply and credit availability.

For instance, an increase in the reserve requirement from 10% to 20% would directly constrain a bank's lending capacity. This is because a higher proportion (20%) of deposits must be held as reserves at the central bank, reducing the pool of funds available for loans. Consequently, the bank can only lend out 80% of deposits compared to the previous 90%.

Higher reserve requirements can also indirectly restrict lending through the interbank market. With a diminished capacity to lend due to increased reserve holdings, banks may become less willing or able to participate in interbank lending. This decline in liquidity within the interbank system can push interbank rates upward. In essence, the reduced lending capacity in the real economy caused by higher reserve requirements can have spillover effects, tightening credit conditions within the interbank market as well.

In contrast, a central bank may opt to lower reserve requirements in response to sluggish economic activity. This policy measure allows banks to hold a smaller portion of deposits as reserves, thereby increasing the pool of funds available for lending. This expansion of credit supply tends to push interest rates downward. Easier and cheaper access to credit becomes more attractive to businesses and consumers, stimulating borrowing and investment. Consequently, economic activity picks up pace. Furthermore, a lower reserve requirement incentivises participation in the interbank market, as banks with excess reserves can lend them out at favourable rates, enhancing overall liquidity within the system.

It's important to remember that reserve requirements are just one tool within a central bank's broader monetary policy framework. This tool can be adjusted to influence the money supply, with the ultimate goal of achieving price stability and fostering sustainable economic growth.

Utilising Macroeconomics

Grasping the intricacies of macroeconomics can be a challenging task. Beyond a basic understanding of its core concepts and market impact, individuals can leverage macroeconomic knowledge to their advantage in the FX market. Hedging strategies represent just one example of this practical application.

Within the FX market, the term "hedging" most commonly refers to utilising offsetting positions in correlated or inversely correlated assets to mitigate risk. However, FX hedging strategies extend beyond this basic concept and encompass a wider range of sophisticated financial instruments and techniques.

Foreign exchange risk is a critical consideration for investors venturing into international markets. Many novice investors may underestimate this risk, overlooking the potential impact of currency fluctuations. As exchange rates change, the cost of hedging strategies can also be affected.

For instance, a UK investor interested in BTP bonds (Italian bonds) would need to convert British pounds to Euros for the purchase and then convert the EUR back to GBP upon exiting the investment. This process exposes the investor to both transaction costs and potential exchange rate volatility that can erode returns.

Let's illustrate this with an example. Imagine an investment in BTP bonds yields a 4% return. However, if the GBP depreciated by 2% against the EUR during the investment period, the net profit would be reduced to 2%. In this scenario, the positive investment return is partially offset by the negative currency movement.

One strategy to mitigate FX volatility involves utilising a currency forward contract or a similar hedging instrument. In this example, the UK investor could borrow Euro at a fixed rate. This fixed exchange rate would shield the investment from potential depreciation of the pound against the Euro. The cost of this hedge, typically quoted as the cross-currency swap rate, reflects the short-term interest rate differential between the two currencies.

While FX hedging offers significant risk mitigation benefits, it's not without its drawbacks. One key consideration is the potential for basis risk. This arises when the hedge instrument's performance deviates from the underlying asset's price movements.

Returning to our previous example, the UK investor hedging against GBP depreciation with a fixed exchange rate contract would be exposed to basis risk. If the Pound strengthens against the Euro instead, the investor would miss out on potential gains from a favourable currency movement. This potential for gains is an inherent trade-off associated with hedging strategies. Professional investors acknowledge this cost as part of the risk management process.

Another potential drawback of FX hedging lies in its complexity. While the basic example of hedging an investment in foreign assets applies in many cases, more sophisticated strategies can be challenging to implement. For instance, hedging an FX position to minimise downside risk during an economic turnaround requires a deep understanding of the dynamic relationships between various markets. Without this knowledge, an investor may construct an ineffective hedge, potentially increasing risk exposure.

Consider an investor holding a long USDJPY position based on the expectation of persistent inflation, prompting potential interest rate hikes by the Federal Reserve. An efficient hedge in this scenario could involve shorting USOIL. The rationale behind this hedge lies in the historical correlation between oil prices and inflation. If inflation expectations materialise, oil prices are likely to rise as well. However, the hedge exposes the investor to basis risk. If the inflation forecast proves inaccurate, the short USOIL position could incur losses. In a scenario where inflation eases and oil prices decline, the Federal Reserve might refrain from raising interest rates. This could lead to a depreciation of the U.S. dollar as investors seek higher returns elsewhere.

This report has provided a glimpse into the interconnectedness of global financial markets and the potential for enhanced portfolio management through FX hedging. The complexities of macro FX hedging strategies offer a vast landscape for further exploration. I look forward to expanding on these concepts in the near future, but for now, that’s a wrap for this week!

The intricacies of macro FX are always fun to write about, let me know what you’d like next!

Great Article